Navigating the world of buy now, pay later financing solutions can be overwhelming, but understanding the Uplift approval requirements gives applicants a distinct advantage. Uplift, a leading provider of installment payments for travel and other big-ticket expenses, sets a clear framework that determines who qualifies for financing. With its streamlined digital application process and commitment to transparency, Uplift has grown rapidly in popularity—especially for consumers looking to spread the cost of vacations, flights, and leisure purchases.

The approval process is designed to be simple but firm, ensuring responsible lending while offering convenience to users. In this guide, we unpack the eligibility criteria, personal data requirements, booking rules, and technical stipulations every applicant must understand before applying.

Personal Information and Identity Verification

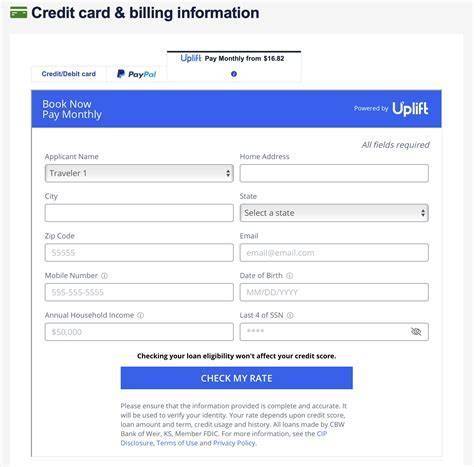

To get started with Uplift, applicants must submit a few essential personal details. These elements are vital for identity verification, fraud prevention, and tailoring credit terms based on individual profiles. At the core, Uplift requires:

- Full Legal Name

- Date of Birth

- Mobile Phone Number

- Social Security Number (SSN) – full SSN or the last four digits, depending on residency and data requirements.

Applicants must be 18 years or older and U.S. residents, which immediately filters out underage and international users from the eligibility pool. The SSN helps validate identity against credit databases, supporting Uplift’s aim to offer customized loan terms responsibly.

The requirement for a valid U.S. mobile phone number and smartphone is not incidental—it is essential. Communication and account verification are mobile-based, so without a connected smartphone, users cannot proceed beyond the initial application stage.

Soft Credit Check: No Impact on Credit Score

One of the more consumer-friendly aspects of Uplift’s process is the soft credit inquiry. This type of check allows the platform to assess an applicant’s financial reliability without impacting their credit score. Unlike hard inquiries, soft pulls are invisible to lenders and do not count against the applicant’s creditworthiness.

Uplift uses this method to determine whether a user qualifies for financing and to offer a real-time credit decision. The system evaluates factors like:

- Credit history

- Existing lines of credit

- Debt-to-income ratio

- Loan repayment habits

While no specific credit score is published as a minimum, users with stronger financial histories tend to receive lower interest rates and larger loan approvals. For those with average credit, Uplift can still offer competitive terms—but possibly with higher APRs or a required down payment.

Minimum Purchase and Booking Window Requirements

The transaction type and timing significantly affect eligibility. Uplift’s model revolves around event-based financing, primarily in the travel and experience economy. For this reason, they enforce minimum purchase requirements:

- $300 minimum for travel-related purchases

- $150 minimum for other qualifying items

Additionally, bookings must be made at least three (3) days prior to departure or event start. This ensures Uplift has adequate time to process payments and allows applicants to repay in installments before the travel or service begins.

This stipulation prevents last-minute bookings using borrowed funds, reducing risk both for Uplift and its partners.

Card Requirements and First Payment Setup

Once approved, applicants must submit valid payment credentials to complete their checkout. Uplift supports only the following card types for the initial transaction setup:

- Visa (credit or debit)

- MasterCard (credit or debit)

- Discover (credit or debit)

The user’s card is charged for either the down payment or first installment, depending on the loan structure offered. This immediate transaction secures the booking or purchase and initiates the repayment timeline. Importantly, prepaid cards and international payment instruments are not accepted, which may exclude certain customer segments.

Interest Rates and Loan Terms

Uplift operates within a flexible interest rate range, offering Annual Percentage Rates (APRs) between 0% and 36%. This range is determined dynamically during the application process and varies based on:

- Applicant’s creditworthiness

- Purchase amount

- Repayment schedule (e.g., 3, 6, 12 months)

Some merchants or seasonal promotions may include 0% APR offers, especially on travel packages or limited-time deals. These offers are still subject to approval, and eligibility depends on the same core criteria outlined earlier.

When interest is applied, the system clearly outlines the monthly payment schedule, total repayment amount, and due dates—a feature that reinforces transparency and customer trust.

Instant Credit Decision and Seamless Checkout Integration

Uplift is embedded directly into partner websites such as airlines, cruise lines, and vacation platforms. This means the entire loan application process happens during checkout, often within seconds. The steps include:

- Selecting Uplift as a payment method

- Submitting required information in the pop-up form

- Receiving an instant approval or decline decision

- Viewing the loan terms and accepting the installment plan

No redirection to third-party portals or long wait times—everything is real-time and automated, allowing users to complete their purchase without disruption.

This seamless integration not only enhances the user experience but also ensures greater data security, as the transaction occurs within the encrypted environment of the partner’s site.

Down Payment Requirements and Repayment Flexibility

Depending on the risk profile of the applicant, Uplift may require a down payment before activating the installment schedule. This upfront cost varies but typically ranges from 10% to 30% of the total cost. The down payment serves as a financial commitment from the borrower and lowers the principal balance for future payments.

Repayments are usually structured as equal monthly payments, with fixed due dates and reminders sent via email or SMS. Users can prepay their loans without penalty, a feature that adds flexibility and supports responsible borrowing.

Automatic payments are encouraged and often set up during the initial loan agreement. This reduces the risk of late fees and ensures consistent repayment habits.

Concurrent Loans and Borrowing Limits

One distinctive feature of Uplift is its policy on multiple active loans. Consumers can hold up to two (2) loans concurrently, provided they remain in good standing. This rule allows frequent travelers or repeat customers to manage multiple trips or experiences simultaneously.

However, Uplift will reevaluate credit eligibility each time a new loan request is made. If an applicant’s credit circumstances have changed, the second loan may be subject to different terms—or may not be approved at all.

This measured approach ensures that consumers do not overextend their financial obligations, promoting sustainable lending behavior.

Conclusion: Transparency, Simplicity, and Responsible Lending

The Uplift approval process is both streamlined and stringent, carefully balancing consumer convenience with responsible credit practices. From soft credit inquiries and minimum purchase thresholds to real-time approvals and loan management tools, Uplift equips users with a powerful financing option—without compromising on transparency.

Understanding these requirements is essential for consumers who want to make informed decisions, avoid surprises during checkout, and maximize the benefits of installment-based travel and event purchases. When used wisely, Uplift can transform large expenses into manageable monthly installments, making dream trips and key life moments more accessible without the burden of immediate full payment.