Aircraft dry leasing continues to be a pivotal mechanism in global aviation finance, offering flexibility and scalability to airlines without the burdens of full ownership. As of April 2025, while precise figures remain elusive beyond September 2024, recent data still provides a comprehensive view into the leasing economics of both narrowbody and widebody aircraft. This article presents an authoritative breakdown of current aircraft dry lease rates, market dynamics, and influential variables that shape pricing across the aviation industry.

Understanding Aircraft Dry Leasing

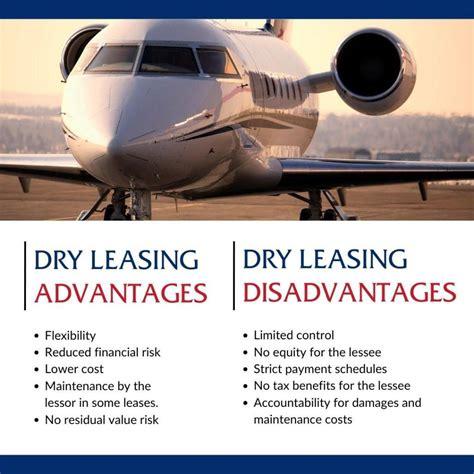

Aircraft dry leasing is a contractual arrangement where an aircraft is leased without crew, maintenance, or insurance (commonly referred to as ACMI). The lessee assumes full operational responsibility, making dry leases popular among established carriers with infrastructure but limited capital for outright aircraft purchases. Unlike wet leases, dry leases are typically long-term agreements, often exceeding 5–8 years in duration.

The strategic value of dry leasing has only grown in an era where cash conservation, fleet optimization, and flexibility in capacity planning are paramount. Airlines use dry leases to expand networks, replace aging fleets, and respond quickly to market demand without incurring the financial risks associated with ownership.

Aircraft Dry Lease Rates in 2024: A Reliable Benchmark

The most recent reliable dataset comes from IBA Group’s Aircraft Values & Lease Rates (September 2024). While these figures precede April 2025, they remain authoritative in the absence of newer, publicly available data. Lease rates are primarily influenced by aircraft age, model generation, and global market demand.

Narrowbody Aircraft Lease Rates

Modern single-aisle aircraft, optimized for short- and medium-haul operations, continue to attract strong demand due to their fuel efficiency and operational versatility.

-

Airbus A320neo: $400,000/month (new)

-

Boeing 737 MAX 8: $400,000/month (new)

-

Airbus A321NX: $460,000/month (new)

-

Airbus A320ceo: $230,000–$250,000/month (mid-life)

-

Boeing 737-800: $230,000–$250,000/month (mid-life)

These models benefit from widespread adoption across low-cost carriers and legacy airlines, ensuring high lease retention and elevated rates for newer variants.

Widebody Aircraft Lease Rates

For long-haul and intercontinental operations, widebody aircraft offer superior passenger capacity and range, reflected in their significantly higher lease valuations.

-

Boeing 787-9: $1,050,000/month (new)

-

Airbus A350-900: $1,140,000/month (new)

-

Boeing 777-300ER: $450,000/month (12 years old)

-

Airbus A330-300: $330,000/month (12 years old)

The lease price differential between new-generation and older aircraft is driven by maintenance costs, fuel burn performance, and residual value profiles. Operators tend to pay a premium for aircraft that deliver lower cost-per-available-seat-kilometer (CASK).

Key Influences on Lease Rates

Lease pricing is not static. It responds dynamically to several interrelated macroeconomic and industry-specific factors:

1. Supply Chain Disruptions

Persistent delays in aircraft production lines, particularly at Boeing and Airbus, have constrained supply. With order backlogs exceeding five years in some cases, lessor inventory becomes a premium asset, driving rates upward.

2. Fleet Retention by Operators

Many airlines opted to extend leases or defer retirements during COVID-19 recovery and geopolitical uncertainty, leading to fewer aircraft being returned to lessors. This reduced the pool of available lease inventory, supporting high prices.

3. Fuel Cost Volatility and ESG Pressures

Aircraft that are more fuel-efficient and environmentally friendly—like the A320neo or 787-9—command higher lease premiums. Airlines are under pressure from investors and regulators to meet sustainability targets, making newer aircraft more attractive despite their higher cost.

Regional Market Trends

North America

Leasing demand remains high among ultra-low-cost carriers (ULCCs) and major U.S. airlines shifting toward younger, leaner fleets. The A321NX and 737 MAX are especially popular in transcontinental domestic routes.

Europe

Airlines like Wizz Air, Ryanair, and Lufthansa Group have increasingly relied on dry leases to standardize their narrowbody fleets. Demand for widebodies remains soft due to slower transatlantic recovery post-pandemic.

Asia-Pacific

A leading growth engine, especially in India and Southeast Asia. Lessor-led fleet expansion has accelerated, with many regional airlines favoring newer aircraft like the A321neo and A320neo.

Market Size vs. Rate Data: A Distinction

While market sizing data from sources like Fortune Business Insights and The Business Research Company offer positive growth projections—$172.88 billion in 2023 to $401.67 billion by 2032—they rarely include granular lease rate specifics.

As of now:

-

Market forecasts suggest a CAGR of 8.8% to 11.1% through 2032.

-

Focus is often on segment splits (dry vs. wet), customer type, and regional penetration.

-

Real-time rate data, such as IBA Group’s September 2024 analysis, remain the most accurate for direct cost assessment.

Limitations of 2025 Lease Data

Efforts to uncover April 2025-specific lease rates through cross-platform searches and databases yielded no newer data sets. The last validated figures from IBA Group’s September 2024 report remain the industry reference. Several commercial sources (e.g., Value Market Research, AirlineGeeks) support broader trends but stop short of publishing aircraft-specific pricing.

This gap illustrates a persistent issue: the opaque nature of leasing contracts and limited public disclosure. Rates fluctuate quickly with market shifts, geopolitical changes, and unexpected supply bottlenecks, but such updates often remain proprietary within lessor–lessee agreements.

Conclusion: What Do Current Rates Mean for Operators?

As of the latest reliable reference point:

-

Narrowbody aircraft lease for $230,000–$460,000/month, with newer models like the A321NX and 737 MAX commanding premium rates.

-

Widebody aircraft lease for $330,000–$1,140,000/month, with the A350-900 topping the scale.

-

Rates reflect aircraft age, performance, market demand, and lessor inventory tightness.

-

Without more recent figures for April 2025, these rates serve as accurate baselines.

Operators should remain agile, monitor real-time market dynamics, and maintain close relationships with leasing companies to respond swiftly to pricing shifts. Dry leasing will remain a foundational tool for fleet modernization and network resilience in the evolving post-pandemic aviation landscape.

Frequently Asked Questions

What is the difference between a dry lease and a wet lease in aviation?

A dry lease includes only the aircraft. The lessee provides the crew, maintenance, and insurance. A wet lease includes all these services, typically arranged by the lessor, and is often used for short-term or seasonal needs.

Why are dry lease rates for newer aircraft higher?

Newer aircraft such as the Airbus A320neo or Boeing 787-9 offer better fuel efficiency, lower emissions, and enhanced reliability. These factors increase demand and residual value, thereby justifying higher monthly lease costs.

How often do aircraft lease rates change?

Lease rates can change quarterly or faster, especially during times of market disruption or supply chain delays. Rates are negotiated between airlines and lessors, often under non-disclosed commercial terms, which limits transparency in real-time rate tracking.