American Express has quietly pulled back the curtain on how its cardmembers actually redeem Membership Rewards points, and the results upend years of conventional wisdom in the points-and-miles world. Despite the loud online culture devoted to extracting luxury flights and aspirational hotel stays, travel redemptions don’t even rank among the top three ways Amex points are used. Instead, the majority of members gravitate toward options that deliver convenience, predictability, and—crucially for Amex—minimal cost per point.

This revelation matters because it exposes a striking divide between points optimizers and everyday cardholders. It also explains why the economics of premium credit cards remain so lucrative, even when issuers appear to give away value at scale.

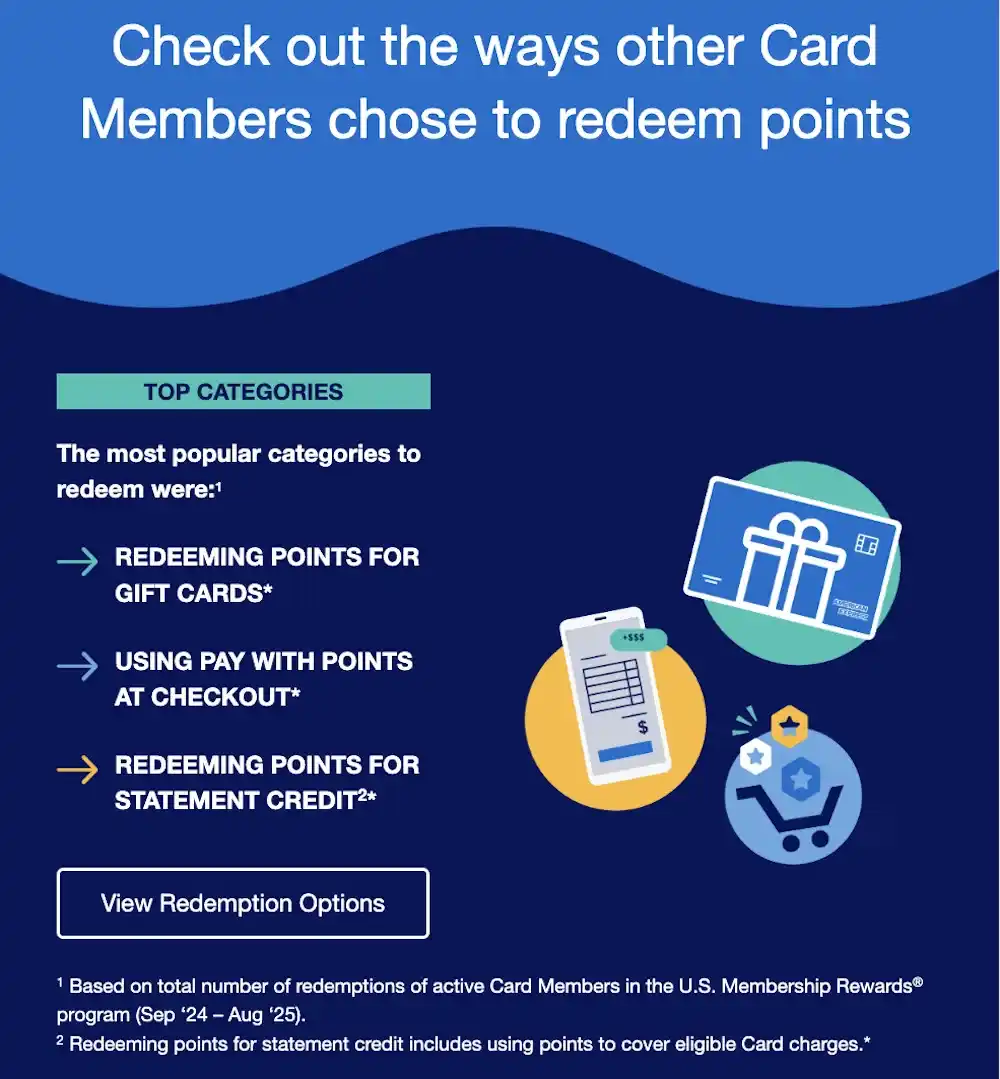

Amex’s Redemption Rankings Tell a Different Story

According to Amex’s own “Points Pulse: Year in Review” data, the most common Membership Rewards redemptions are gift cards, paying with points at checkout, and statement credits. Each of these options delivers a fixed value of roughly 0.6–0.7 cents per point, a rate that seasoned travelers would consider painfully inefficient. Yet these methods dominate real-world usage.

The implication is blunt: most Amex cardmembers treat points like cash, not like a strategic asset. They redeem when it’s easy, visible, and emotionally frictionless, not when it maximizes theoretical value. Gift cards feel tangible. Statement credits feel responsible. Paying with points at checkout feels seamless. Transferring points to airline partners, by contrast, feels abstract, complex, and risky.

By the time the average consumer encounters blackout dates, award charts, or transfer ratios, the psychological cost outweighs the perceived reward.

Why Travel Redemptions Remain a Niche Behavior

Among enthusiasts, Amex points are often valued at 1.5 to 2 cents each, sometimes more, thanks to premium cabin flights and international business-class redemptions. That value only materializes when points are transferred to airline or hotel partners, a process that requires planning, flexibility, and a tolerance for arcane rules.

The data makes clear that this group is a minority. Most cardmembers do not track cents-per-point valuations. They do not stockpile points for aspirational trips. They redeem opportunistically, often as soon as balances feel “large enough” to be useful.

This gap between perceived value and realized value is where Amex quietly wins. When points are redeemed at under one cent each, the company fulfills its rewards promise at a fraction of the cost that travel redemptions can impose.

The Hidden Math Behind Credit Card Profitability

Credit card issuers generate revenue primarily through interchange fees, annual fees, and financing charges. Rewards are a cost center, but one that can be carefully controlled. When a cardmember redeems points for a statement credit worth 0.6 cents per point, Amex’s expense is tightly capped.

Travel redemptions tell a different story. When points are transferred to airline or hotel partners, Amex often pays significantly more—sometimes around 1.5 cents per point or higher, depending on the partner and agreement. From a pure accounting perspective, a customer who consistently transfers points for high-value redemptions may be far less profitable than one who redeems casually.

This creates a fascinating inversion. The most knowledgeable customers are often the least lucrative, while the least optimized behaviors quietly subsidize the entire rewards ecosystem.

Convenience Always Beats Optimization at Scale

From a behavioral economics standpoint, the findings are not surprising. Humans consistently favor certainty over complexity, even when complexity offers higher upside. A guaranteed $60 statement credit today feels more “real” than the possibility of $170 in flight value months from now.

Amex understands this deeply. Redemption interfaces are designed to make low-value options prominent and effortless, while transfers require deliberate action. This is not deception; it’s alignment with how most people prefer to interact with money.

For Amex, the result is ideal. The brand markets aspirational travel, but profits from mundane redemption habits. Luxury imagery drives sign-ups, while everyday behavior protects margins.

What This Means for Cardmembers—and Competitors

For consumers who truly want cash-like rewards, the irony is sharp. A 0.6–0.7% effective return is easily beaten by no-frills cash-back cards offering 2% or more, with no mental gymnastics required. Yet brand loyalty, perceived prestige, and habit keep many cardmembers locked into suboptimal value.

Competitors like Bilt, whose customer base skews heavily toward point transfers and bonus-driven redemptions, face a very different economic challenge. Their users are more sophisticated—and more expensive. Amex, by contrast, benefits from scale and behavioral inertia.

The Quiet Lesson Inside the Numbers

The real takeaway isn’t that travel redemptions are overrated. It’s that they are culturally loud but statistically rare. Online discourse magnifies the behavior of a small, highly engaged group, while millions of everyday users quietly redeem points in ways that favor simplicity over strategy.

Amex’s data is a reminder that markets are shaped less by optimal behavior and more by typical behavior. In that sense, the fact that travel doesn’t crack the top three redemptions isn’t shocking—it’s inevitable. The wild part is how long the myth of universal optimization managed to survive.