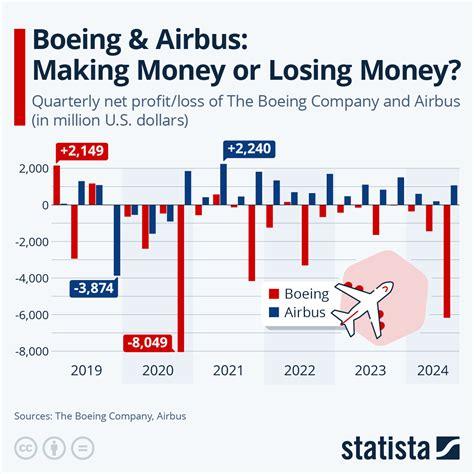

The global aerospace industry has entered a striking new phase, one defined not by steady dominance but by sharp reversals and fragile recoveries. Airbus, long seen as the more stable of the two manufacturing giants, has reported a staggering 52% drop in profits for the first quarter of 2026. At the same time, Boeing is mounting a determined comeback, steadily restoring production strength and reclaiming lost ground in aircraft deliveries.

This sudden imbalance is not merely a quarterly anomaly—it is a revealing snapshot of how deeply supply chain vulnerabilities, engine shortages, and production bottlenecks can reshape the competitive landscape. Beneath the numbers lies a far more consequential story: one of structural strain inside Airbus and a cautiously optimistic resurgence from its American rival.

Airbus Financial Shock: A 52% Profit Decline Explained

Airbus entered 2026 with confidence rooted in its record-breaking order backlog, yet the first quarter delivered a harsh reality check. The company’s adjusted operating profit plunged from €624 million to €300 million, a drop that underscores how operational disruptions can outweigh even the strongest demand signals.

Deliveries, the lifeblood of aircraft manufacturing revenue, fell 16% year-on-year, landing at just 114 aircraft. This decline is particularly painful because revenue recognition in aerospace depends heavily on completed deliveries rather than production milestones. In other words, aircraft sitting unfinished—or worse, engineless—translate directly into delayed cash flow and financial strain.

The unusually candid tone from CEO Guillaume Faury, who admitted that “we are suffering,” reflects internal pressure rarely voiced so openly. Airbus is not facing a demand problem—it is grappling with a conversion problem, where orders fail to translate into deliveries at the expected pace.

The Engine Crisis Crippling Airbus Production

At the heart of Airbus’s struggles lies a bottleneck that has proven both persistent and costly: the Pratt & Whitney Geared Turbofan (GTF) engine crisis. These engines power a significant portion of the A320neo family, Airbus’s flagship narrowbody aircraft.

Pratt & Whitney continues to prioritize repairs for over 550 grounded aircraft worldwide, diverting resources away from new engine production. The result is a severe shortage that leaves freshly assembled Airbus jets stranded on factory floors, unable to be delivered.

This situation creates a paradox that would be almost ironic if it weren’t so expensive: Airbus is producing aircraft but cannot deliver them, effectively locking billions of euros in inventory limbo. The mismatch between production capability and delivery readiness is eroding profitability at a critical moment.

The company is pushing aggressively toward a target of 75 A320-family aircraft per month, yet without sufficient engines, that ambition risks becoming an exercise in accumulation rather than execution.

Boeing’s Recovery Gains Real Momentum

While Airbus wrestles with constraints, Boeing is quietly rebuilding its operational rhythm. After years of crisis management stemming from the 737 MAX grounding and production halts, the American manufacturer is showing tangible signs of recovery.

In the first quarter of 2026, Boeing delivered 143 aircraft, surpassing Airbus for the first time since 2018. This milestone carries symbolic weight—it marks not just a quarterly win, but a turning point in Boeing’s long rehabilitation process.

Production of the 737 MAX has stabilized, reaching 42 aircraft per month, with plans to scale up further to 52. Meanwhile, the 787 Dreamliner program continues to provide consistent output and revenue, acting as a stabilizing force within Boeing’s widebody segment.

The lifting of regulatory production caps by the FAA has also played a crucial role, allowing Boeing to accelerate output without the constraints that previously throttled its recovery. This newfound flexibility is translating directly into stronger delivery performance and improving financial outlooks.

A Narrowbody Battle Far From Over

Despite Boeing’s recent gains, the broader competitive landscape remains tilted in Airbus’s favor—at least for now. The A320 family has surpassed the Boeing 737 as the most-delivered commercial aircraft in history, with over 12,260 total deliveries.

More importantly, Airbus holds a commanding lead in backlog, with over 7,100 orders compared to Boeing’s roughly 4,800. This backlog acts as a long-term buffer, ensuring sustained demand even as short-term execution falters.

However, Boeing is not without its strategic weapons. The upcoming certification of the 737 MAX 7 and MAX 10, expected later in 2026, could significantly strengthen its position. The MAX 10, in particular, targets the highly successful A321neo, Airbus’s most profitable narrowbody variant.

Still, reclaiming dominance in this segment is not a short-term project. It is, quite literally, a decade-long contest, shaped by production scalability, certification timelines, and airline fleet strategies.

Widebody Dynamics: Stability Meets Opportunity

In the widebody market, the dynamics are more balanced, though not without nuance. Boeing’s 787 Dreamliner continues to perform strongly, providing steady deliveries and maintaining customer confidence. This program has been a critical financial anchor during turbulent years.

At the same time, delays in the 777X program have opened a window of opportunity for Airbus. The European manufacturer has capitalized on this gap, driving sales of the A350 and sustaining interest in the A330neo.

Even with Boeing’s higher overall widebody sales volume, Airbus is managing to extract solid profitability from its lineup. This balance highlights an important truth: market leadership is not solely about volume, but also about program efficiency and margin performance.

The Real Risk: Supply Chain Fragility

What this unfolding situation ultimately exposes is the fragility of the aerospace supply chain. Aircraft manufacturing is an intricate ecosystem where delays in a single component—especially something as critical as an engine—can ripple across the entire production cycle.

Airbus’s current predicament is not due to mismanagement or lack of demand, but rather its dependence on external suppliers operating under extreme pressure. This dependency raises strategic questions about vertical integration, supplier diversification, and risk mitigation.

For Boeing, the lesson is equally clear. Its recovery, while encouraging, remains vulnerable to similar disruptions. The difference is timing: Boeing is ascending while Airbus is constrained, creating a temporary but meaningful shift in competitive momentum.

A Pivotal Year for Aviation Giants

The events of early 2026 are shaping up to be more than a quarterly fluctuation—they represent a pivotal inflection point for both Airbus and Boeing. Airbus must resolve its engine bottleneck quickly to prevent prolonged financial drag, while Boeing must maintain discipline to avoid repeating past missteps.

The race is no longer defined solely by innovation or order books. It is increasingly about execution under pressure, the ability to convert demand into delivered aircraft efficiently and consistently.

As the year progresses, one question looms large: will Airbus stabilize and reassert its dominance, or will Boeing capitalize on this opening to permanently narrow the gap? The answer will not just define 2026—it will shape the trajectory of the global aviation industry for years to come.