The question “how many aircraft are scrapped every year” sounds deceptively simple, but the answer reveals a complex and evolving picture shaped by economics, engineering lifecycles, global crises, and even the hidden value of aircraft engines. At present, the aviation industry sits in a peculiar moment—demand for aircraft is surging, yet retirements are unusually suppressed. This tension is redefining what “retirement” really means in modern aviation.

In typical conditions, the global aviation ecosystem operates on a predictable rhythm: aircraft are delivered, flown for decades, and eventually retired and dismantled. However, that rhythm has been disrupted. Supply chain bottlenecks, engine shortages, and delayed production schedules have forced airlines to hold onto aging aircraft far longer than expected. As a result, the number of aircraft scrapped annually is temporarily lower than historical norms, masking a much larger wave of retirements building beneath the surface.

Today, estimates suggest that around 500 commercial aircraft are scrapped each year, although some analyses place the figure closer to 650 depending on definitions and inclusions. This number is expected to rise significantly—potentially reaching 800 to 900 aircraft annually by the late 2020s and early 2030s—as a backlog of aging fleets finally begins to clear.

Why Aircraft Retirement Numbers Are Lower Than Expected Today

The current dip in aircraft retirements is not due to a lack of aging planes. In fact, quite the opposite is true. The world is facing a massive aircraft delivery shortfall, estimated at around 5,300 aircraft, while airlines collectively have approximately 16,000 planes on order. This imbalance has forced carriers into a holding pattern—literally and financially.

Airlines that would normally retire older jets are instead extending their service lives. Widebody aircraft such as the Boeing 747-8, Airbus A380, and older Boeing 777 variants are staying active longer than planned. These aircraft are not necessarily efficient by modern standards, but they remain indispensable due to a simple reality: there are not enough new planes to replace them.

The situation becomes clearer when comparing production timelines. In 1995, the combined output of Boeing, Airbus, and McDonnell Douglas was just 376 aircraft. Fast forward to 2025, and total deliveries have surged to around 1,500 aircraft annually. Because aircraft typically serve for 25 to 30 years, today’s retirement figures are still catching up with the lower production volumes of the past.

This lag effect means that retirement rates today reflect the smaller fleets of the 1990s, not the massive expansion seen in the 2000s and beyond. When those newer aircraft begin reaching retirement age en masse, the numbers will climb sharply.

The Lifecycle of a Commercial Aircraft: When Does Scrapping Begin?

Aircraft are engineered for longevity, but not immortality. Most commercial jets are retired between 25 and 30 years of service, though this varies depending on usage, maintenance quality, and market conditions. Narrowbody aircraft—like the Airbus A320 or Boeing 737—often retire slightly earlier due to higher utilization rates, while widebodies can remain in service longer.

Freighter aircraft, especially those converted from passenger jets, often extend their lifespan to 30–40 years, squeezing additional value from aging airframes. However, retirement is rarely a single, clearly defined moment. Instead, it unfolds in stages: withdrawal from service, storage, part-out, and finally dismantling.

This ambiguity complicates any attempt to produce an exact global retirement figure. An aircraft parked in a desert storage facility may technically still exist in an airline’s inventory, even if it never flies again. Others are written off after accidents, raising questions about whether they should be counted as “retired” or “lost.”

Global Shocks That Reshape Aircraft Scrapping Rates

Few industries are as sensitive to global events as aviation, and aircraft retirement patterns reflect that volatility. The COVID-19 pandemic triggered one of the most dramatic shifts in aviation history, leading to a sudden wave of retirements. Airlines grounded fleets overnight and accelerated the phase-out of inefficient aircraft.

Notably, carriers like Air France retired their Airbus A380 fleets early, despite the aircraft being relatively young by industry standards. The pandemic provided a rare opportunity to reset fleet strategies without the usual operational constraints.

Earlier crises have had similar effects. The aftermath of September 11, 2001, suppressed air travel demand for years, slowing deliveries and influencing retirement decisions. More recently, ongoing supply chain disruptions and production delays—particularly affecting Boeing’s 737 MAX and 787 programs—have once again altered the balance between deliveries and retirements.

According to industry analysis, aircraft retirement rates between 2024 and 2026 are expected to be approximately 24% lower than pre-pandemic levels, highlighting just how unusual the current environment is.

When Scrapping Happens for Unexpected Reasons

While age and efficiency are the primary drivers of aircraft retirement, some retirements occur under far more unusual circumstances. Accidents, regulatory actions, and sudden shifts in component values can all push aircraft out of service prematurely.

A striking example emerged in 2025, when a crash involving a McDonnell Douglas MD-11 cargo aircraft led to the grounding of the entire fleet. In response, UPS accelerated the retirement of around 30 MD-11s, accounting for roughly 6% of global aircraft retirements that year. Such concentrated retirements can significantly skew annual totals.

Even more surprising is the role of engine economics. In today’s market, aircraft engines—particularly those in short supply—can be more valuable than the aircraft themselves. The well-documented issues with Pratt & Whitney’s GTF engines have created a scarcity that has flipped traditional valuation models.

As a result, some relatively new aircraft, including three-year-old Airbus A320neo jets, have been dismantled primarily to harvest their engines. This phenomenon would have been almost unthinkable a decade ago, yet it underscores how component scarcity can override conventional lifecycle expectations.

The Blurred Line Between Storage and Retirement

One of the most persistent challenges in answering how many aircraft are scrapped each year lies in defining what “scrapped” actually means. Aircraft can spend years—or even decades—in storage before being formally dismantled.

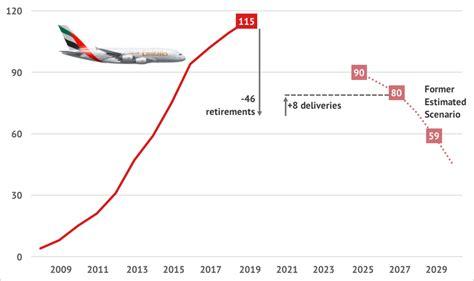

During the pandemic, airlines like Emirates parked large portions of their Airbus A380 fleets. Some of these aircraft may eventually return to service, while others may never fly again. The uncertainty creates a gray zone where aircraft exist in limbo, neither active nor officially retired.

This ambiguity extends to regions affected by sanctions or financial constraints. In countries like Iran, numerous aircraft sit grounded due to limited access to spare parts and maintenance resources. Similarly, certain fleets in Russia have faced operational challenges due to sanctions, leaving aircraft stranded in extended inactivity.

From a statistical perspective, these aircraft complicate retirement counts. Are they retired, stored, or simply paused? The answer often depends on the methodology used by analysts, which is why reported figures can vary significantly.

What Happens When Aircraft Are Scrapped?

When an aircraft finally reaches the end of its operational life, it enters a highly specialized recycling process. Contrary to popular imagination, scrapping is not simply about dismantling metal—it is about maximizing the recovery of valuable components.

Modern aircraft are designed with recyclability in mind. Up to 90% of an aircraft’s materials can be recovered and reused, including aluminum, titanium, and high-value avionics systems. However, the most prized assets are typically engines, landing gear, and other high-cost components.

Airlines and leasing companies often engage in “part-out” strategies, where aircraft are acquired specifically to supply spare parts. This approach can be more cost-effective than sourcing new components, particularly for older or out-of-production models.

A notable example is Delta Air Lines, which acquired over 100 Boeing 717 aircraft not just for operation but also to sustain its active fleet through parts harvesting. This strategy reflects a broader industry trend where retired aircraft continue generating value long after their final flight.

The Future: A Surge in Aircraft Scrapping Ahead

While current retirement numbers appear modest, the future tells a different story. The aviation industry is on the cusp of a significant shift driven by decades of fleet expansion. Aircraft delivered in the early 2000s—during a period of rapid growth—are now approaching retirement age.

By the 2030s and 2040s, the number of aircraft reaching end-of-life will increase dramatically. Boeing forecasts that the world will require nearly 44,000 new aircraft between 2024 and 2043, implying a corresponding surge in retirements as older fleets are replaced.

This growth will fuel the expansion of the aircraft recycling industry, which is projected to grow from $5.06 billion in 2025 to $7.78 billion by 2031. Meanwhile, Airbus estimates that dismantling and recycling activities could generate $52 billion in recoverable material value over the next two decades.

The implications extend beyond economics. As sustainability becomes a central concern, efficient recycling processes will play a critical role in reducing aviation’s environmental footprint. The industry is increasingly focused on developing methods to recycle composite materials and reduce waste, ensuring that future retirements are not just profitable but also environmentally responsible.

A Moving Target: Why the Exact Number Will Always Vary

Ultimately, the number of aircraft scrapped each year is not a fixed figure but a moving target influenced by a web of interconnected factors. Definitions vary, methodologies differ, and real-world events constantly reshape the landscape.

What remains clear is the broader trend: aircraft retirements are temporarily suppressed but poised for significant growth. As supply chains recover and new aircraft deliveries accelerate, airlines will finally begin retiring older fleets at scale.

The result will be a sharp increase in scrapping activity—one that reflects not just the aging of aircraft, but the evolution of an entire industry adapting to new technologies, economic realities, and environmental expectations.

In that sense, the question is not just how many aircraft are scrapped every year, but what those numbers reveal about the state of global aviation. And right now, they tell a story of delay, adaptation, and an approaching wave that will redefine the skies for decades to come.