In May 2025, the U.S. domestic air travel market experienced its fourth consecutive month of decline, marking a concerning trend in a sector that had otherwise shown signs of pandemic-era recovery. According to data released by the International Air Transport Association (IATA), demand measured in Revenue Passenger Kilometers (RPK) dropped 1.7% year-over-year, reflecting a broader economic slowdown gripping the United States. While the world’s largest aviation market stumbles, global air travel has accelerated, underscoring a growing divergence between U.S. domestic weakness and global aviation strength.

U.S. Domestic Air Travel Faces Prolonged Weakness

Despite increasing capacity by 2% compared to May 2024—measured in Available Seat Kilometers (ASK)—U.S. airlines witnessed a 3.1 percentage point drop in passenger load factor, settling at 83%. This underperformance signals not only an oversupply of seats but also a softening of consumer and corporate travel sentiment, driven by ongoing concerns around inflation, economic uncertainty, and reduced federal government travel spending.

The federal travel cutbacks, which form a significant share of U.S. air traffic, mirror a broader shift toward fiscal restraint within government agencies. Coupled with waning consumer confidence, the private sector is also reining in business travel, cautious of cost efficiency amid murky economic forecasts. This dual-pronged reduction in demand—both public and private—is dampening airline profitability and pushing carriers to reassess their capacity and pricing strategies.

Global Air Travel Soars with International Demand Leading the Charge

While the U.S. faces contraction, the global air travel sector surged ahead with an impressive 5% year-over-year growth in May 2025. This was primarily powered by international traffic, which rose 6.7% compared to May 2024. The international passenger load factor climbed slightly to 83.2%, the highest ever recorded in May—a clear indication that travelers are increasingly returning to long-haul routes.

Emerging markets and recovering regions like Asia-Pacific and Latin America were the key engines behind this growth. Their strong post-pandemic rebound, coupled with high consumer travel demand, has solidified the momentum of the global aviation sector even as the North American market lags.

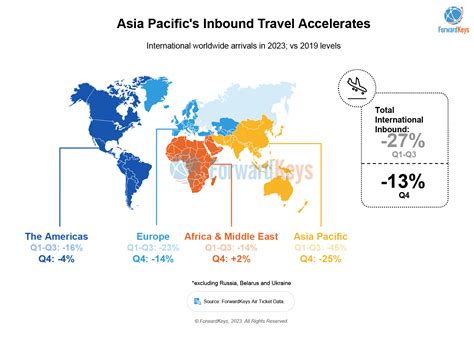

Asia-Pacific and Latin America Drive the Global Recovery

Among all regions, Asia-Pacific led with a 13.3% rise in international air travel demand, demonstrating the region’s robust and sustained recovery. Countries such as China, India, and Japan saw exceptional growth as easing restrictions and pent-up demand fueled passenger numbers. This surge is reflective of broader macroeconomic stability and high levels of consumer mobility within the region.

In Latin America, the story was similarly positive. The region saw a 7.5% increase in demand and a 9.6% rise in capacity, with Brazil alone posting an 18.3% jump in traffic. Airlines across Latin America are rapidly expanding routes and frequency, capitalizing on growing middle-class travel and strong summer season demand.

Meanwhile, Africa reported a 9.5% growth in demand, a promising sign for regional carriers still navigating post-pandemic restructuring. On the opposite end, Japan was the only major country to report a decline in available seat kilometers, down 1.1%, as its carriers recalibrate after initial overexpansion.

Geopolitical and Economic Tensions Still Loom Over Aviation

Despite encouraging global figures, the aviation sector remains vulnerable to geopolitical shocks and fuel price volatility. In late June 2025, escalating tensions in the Middle East raised alarms across global markets. Although fuel prices stayed relatively low throughout May, there is no guarantee they will remain stable, particularly if regional conflicts intensify.

IATA Director General Willie Walsh emphasized the lingering risks associated with geopolitical instability, which can disrupt travel patterns, strain supply chains, and trigger abrupt cost escalations for airlines. These dynamics add another layer of complexity to an industry that is still navigating pandemic aftershocks.

U.S. Airlines Under Pressure to Recalibrate Strategies

With demand sliding and aircraft going out with empty seats, U.S. carriers face growing pressure to adjust. Route optimization, strategic pricing, and refined capacity management are emerging as critical levers. Many airlines are now reevaluating their domestic versus international route mix, betting that transatlantic and intercontinental markets may offer better returns in the coming months.

The persistently low load factors in domestic operations are also prompting questions about the sustainability of recent fleet expansions and infrastructure investments made under the assumption of steady growth. If the U.S. economy continues to soften, the ripple effect could further suppress demand in Tier-2 and Tier-3 cities where air travel is often discretionary.

Peak Travel Season Offers a Glimmer of Hope

Amid the domestic gloom, forward bookings for the Northern Hemisphere’s summer peak season provide some hope. Airlines are reporting steady international ticket sales, with popular European and Asia-Pacific destinations showing high reservation rates. This uptick may offer temporary relief to major carriers, provided operational efficiencies are maintained and geopolitical risks don’t spike.

Additionally, business travel may begin to rebound slightly as corporate fiscal calendars reset mid-year, though the pace remains uncertain. For now, leisure travel remains the backbone of global demand, with millennials and Gen Z driving international travel trends despite economic anxiety.

Strategic Outlook: Adjusting to a Two-Speed Recovery

What emerges from the May 2025 data is a tale of two markets: one domestic, stagnating under economic pressure, and one global, rebounding with resilience. The discrepancy underscores the need for region-specific strategies. North American airlines must focus on:

- Dynamic route management to match actual demand

- Agile pricing models that respond to rapid economic shifts

- Enhanced operational efficiency to protect margins

Conversely, carriers in high-growth regions will likely continue expanding fleet capacity, improving airport infrastructure, and strengthening intercontinental connectivity.

The divergence also places pressure on global alliances such as Oneworld, SkyTeam, and Star Alliance to realign codeshare agreements and maximize efficiency across uneven recovery curves. Airlines that can balance this dual reality—cautious at home, aggressive abroad—will likely emerge stronger in the evolving aviation landscape.

Conclusion: A Complex but Navigable Horizon

The May 2025 aviation snapshot reflects a complex mix of contraction and expansion, offering no single narrative but rather a mosaic of region-specific dynamics. The U.S. domestic market, once a bellwether of global air travel health, is now a cautionary tale in economic fragility. In stark contrast, global travel, led by Asia-Pacific, Latin America, and parts of Africa, continues to chart a promising path toward full recovery.

For airlines, investors, and policymakers, the lesson is clear: the future of aviation lies in flexibility, agility, and precision planning. As summer travel crests and the world watches whether North America can rebound, one certainty remains—the skies beyond U.S. borders are busier than ever.