The U.S. hotel construction volume has hit a staggering low, now standing at its lowest point in 20 quarters, according to the latest data from CoStar. This significant downturn, which has persisted for six consecutive months, marks a dramatic shift from the robust hotel development trends observed just a year ago. As the hospitality industry grapples with a myriad of challenges, including weakened demand, soaring construction costs, and relentless economic uncertainty, the pipeline for new hotel projects across the country is being systematically scaled back. The number of hotel rooms currently under construction has plummeted by nearly 12 percent compared to the same time last year, highlighting a concerning trend that signals deeper issues within the industry.

The decline in construction activity is alarming, especially as it represents the longest period of sustained downturn in hotel development since the pandemic’s initial impact on the market. The broader economic landscape, characterized by high inflation and global supply chain disruptions, has escalated costs associated with building materials and labor, creating a perfect storm for the hospitality sector. As developers continue to face these headwinds, the outlook for new projects remains bleak, raising questions about the future of hotel construction in the United States.

Impact of Economic Uncertainty on Hotel Construction

Economic uncertainty lies at the heart of the current slump in hotel construction. Real estate owners are increasingly wary of the risks involved in investing in the hospitality market, which has been subject to significant volatility due to fluctuating economic conditions. The aftermath of the global pandemic has further complicated matters, drastically impacting travel demand and the overall economy. Many hotel developers find themselves contending with a crucial challenge: securing financing for new projects has become more difficult as credit has tightened and interest rates have risen. The Federal Reserve’s rate hikes, implemented in response to ongoing inflation, have dampened developers’ enthusiasm for embarking on ambitious building projects.

Moreover, the escalating costs of construction—driven by labor shortages and material price increases—have discouraged lodging investors from proceeding with new hotel developments. Developers are struggling to keep their projects on budget, leading to delays, cutbacks, or even cancellations. This confluence of factors is creating a tense atmosphere in the hotel development sector, where uncertainty reigns supreme.

Regional Trends: Southern U.S. Dominates Hotel Development

While overall hotel construction is on the decline, the Southern United States emerges as a beacon of hope for new hotel projects. This region is currently leading the charge in new hotel supply, according to industry sources. Cities such as Dallas, Houston, and Atlanta are experiencing a surge in hotel development, primarily in secondary and tertiary markets, which indicates a strategic retreat from traditional major urban centers.

Several factors contribute to the Southern U.S.’s robust hotel construction landscape. Strong local economies, consistent tourism influxes, and a rise in business travel are driving demand in these areas. Additionally, as populations in these cities continue to grow due to an influx of residents seeking affordable living options, the need for hotel accommodations is becoming more pronounced. This trend signifies that hotels in smaller markets are likely to benefit from the ongoing relocation of businesses and individuals to the South.

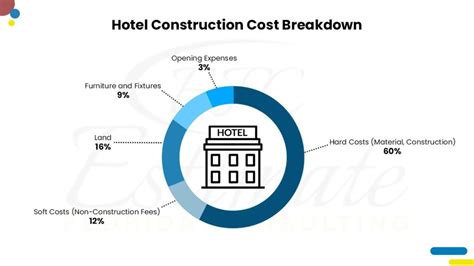

Factors Contributing to the Decline in Hotel Construction

The downward trajectory in hotel construction can be attributed to several critical factors that inhibit progress in the industry. These include:

- Lower Hotel Demand: The unpredictable nature of travel habits during times of economic instability has resulted in uneven demand for hotel accommodations. Although some regions report high occupancy rates, the overall demand for travel has yet to fully rebound to pre-pandemic levels, leaving builders cautious about new investments.

- Ongoing Economic Volatility: The global economic landscape remains fraught with uncertainty, affecting the profitability prospects of new hotel ventures. The industry is particularly sensitive to fluctuations in key economic indicators such as inflation, interest rates, and consumer spending.

- Rising Construction Costs: With labor and material costs consistently climbing, developers are finding it increasingly challenging to complete projects within budget constraints. As expenses soar, new hotel constructions face significant hurdles, as the demand for high-quality builds contrasts sharply with the lower tolerance for subpar outcomes.

JD Power’s 2025 Hotel Guest Satisfaction Index

In the midst of a cooling construction environment, the hotel industry is simultaneously exploring innovative ways to assess and enhance guest satisfaction. According to JD Power’s 2025 Hotel Guest Satisfaction Index for North America, several hotel chains excelled across various segments. Notably, The Ritz-Carlton emerged as the frontrunner in the Luxury category, while Omni Hotels & Resorts took the top spot in the Upper-Upscale category. Other notable winners included Drury Hotels, which ranked first in the Upscale category, and Hyatt House, recognized for its excellence in the Upscale Extended Stay category for the fourth consecutive year. These accolades underscore the industry’s commitment to maintaining high service standards, even as construction slows.

Key Hotel Developments Amid Construction Slowdown

Despite the overarching decline in hotel construction, there are still noteworthy developments taking shape within the market. Among these are:

- Portman Holdings is set to develop the Marriott Convention Center Hotel in Cincinnati, located south of the Duke Energy Convention Center. This ambitious project is scheduled to open in 2028 and will feature 700 rooms, over 62,000 square feet of meeting space, and a 17,445-square-foot events terrace.

- The REMI Scottsdale in Arizona, part of the Autograph Collection, is slated to begin welcoming guests in July 2025. This property will boast five dining venues curated by the Alliance Hospitality Group.

- The TownePlace Suites by Marriott recently launched a new extended-stay hotel in Bozeman, Montana, featuring 107 suites along with a bar and restaurant.

Although the pace of hotel construction has cooled significantly, these developments indicate a persistent interest in expanding the hotel market, particularly in locations that prioritize conventions and tourism.

Outlook for U.S. Hotel Construction

Looking ahead, the future of hotel development in the United States remains somewhat ambiguous in light of rising construction costs and ongoing economic uncertainty. Nevertheless, there is reason for cautious optimism. The long-term potential of the market may be bolstered by stable demand in southern states and select urban centers, alongside an increasing focus on hotel renovations and the repositioning of existing properties. This slowdown in new hotel development could also stimulate greater investment in refurbishments and upgrades, allowing current hotel owners to maintain competitiveness as they navigate the challenging landscape.

In summary, while the U.S. hotel construction sector faces significant challenges, the adaptability and resilience of the industry suggest that it may find ways to thrive amidst adversity. As stakeholders await a clearer economic picture, the focus on quality, guest satisfaction, and strategic development will be crucial in shaping the future of hotel construction in America.