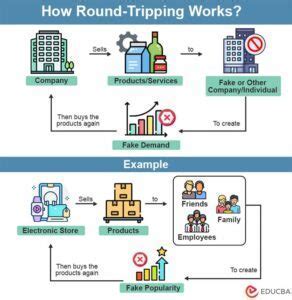

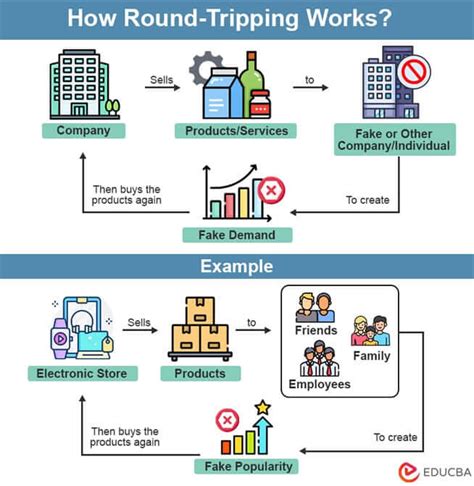

Round-trip transactions, while deceptively innocuous in appearance, represent one of the most insidious forms of corporate financial misrepresentation. These transactions involve the movement of funds or assets between two entities—often the same parties cyclically—without any genuine economic benefit or change in ownership. Their core purpose is to inflate revenues, manipulate balance sheets, or mislead investors and regulatory bodies. This practice has emerged in several high-profile scandals and remains a focus of forensic accounting and regulatory oversight today.

The essence of round-tripping lies in its ability to simulate business activity where none truly exists. For instance, a company may sell an asset to a partner firm with the hidden agreement to repurchase it shortly thereafter. No real value is created, yet the transaction can be recorded as revenue. In more elaborate schemes, shell companies or related-party entities are used to obscure the circular nature of these dealings.

The Real Cost: Consequences of Round-Tripping

Engaging in round-trip transactions can have devastating consequences. Once uncovered, companies often face regulatory investigations, criminal and civil lawsuits, heavy financial penalties, and irreparable reputational damage. Investors lose trust, share prices plummet, and executives may face jail time. Moreover, misleading financial statements disrupt capital market integrity, undermining the foundation of investor confidence.

Historically, firms like Enron and AOL-Time Warner were involved in such schemes, using round-tripping to mask poor performance and inflate earnings reports. The exposure of these tactics resulted in billions in shareholder losses and triggered reforms like the Sarbanes-Oxley Act.

Red Flags: How to Spot Round-Trip Transactions

While round-tripping schemes are often designed to avoid detection, they tend to leave behind identifiable financial anomalies. Understanding these red flags can help analysts, auditors, and regulators proactively identify suspicious activities:

- Unusually consistent revenue growth, even during market downturns

- High sales volume with minimal change in receivables, suggesting fictitious revenue recognition

- Repeated transactions with the same entity, especially if they lack clear business rationale

- Significant sales spikes at period end, likely to manipulate quarterly results

- Low gross margins despite high reported revenue

- Unusual inventory levels, inconsistent with operational trends

- Cash flow mismatches, where profits are reported without corresponding cash inflows

These inconsistencies, when occurring together, often indicate fabricated transactions meant to inflate a company’s financial health.

Detecting Deception: Methods of Financial Analysis

Forensic investigators and financial analysts deploy detailed comparative analysis to uncover the truth behind suspicious transactions. The process often includes:

- Comparing sales patterns against industry norms to detect unnatural growth

- Evaluating accounts receivable trends in proportion to reported revenue

- Scrutinizing related-party transactions, especially those involving shell entities or off-book arrangements

- Assessing the alignment between inventory levels and sales claims

- Investigating cash flow statements, which often reveal irregular inflows not justified by legitimate operations

Each of these steps requires granular insight into the company’s operations and access to supporting documentation such as contracts, invoices, and intercompany agreements.

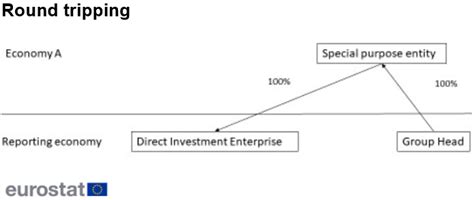

Round-Tripping in Global Capital Markets

Beyond corporate financials, round-tripping also manifests in capital markets, often in the context of tax evasion and foreign direct investment (FDI) manipulation. Entities exploit low-tax jurisdictions and offshore accounts to hide the origin of funds. Common tactics include:

- Routing money through shell companies registered in tax havens

- Using falsified invoices or receipts to justify transactions

- Initiating fictitious loans or investments between shell companies and parent firms

- Employing circular funding structures that create the illusion of external capital inflow

These techniques can disguise illicit capital flows, launder money, or evade taxation, creating substantial challenges for global regulators and financial intelligence units.

Preventing and Mitigating Round-Tripping Schemes

To safeguard organizations from round-tripping, robust internal controls and regulatory compliance frameworks must be implemented. Key prevention strategies include:

- Establishing segregation of duties to avoid conflict of interest in transaction approvals

- Mandating formal approval procedures for all large or unusual transactions

- Implementing real-time transaction monitoring systems that flag irregularities

- Conducting frequent internal and external audits, with special emphasis on related-party dealings

- Performing comprehensive due diligence on counterparties to validate legitimacy and business purpose

- Training employees to identify signs of accounting manipulation and promoting ethical conduct

Organizations that prioritize transparency, accountability, and auditability are far less susceptible to the risks posed by fraudulent financial schemes.

Round-Tripping in Trading and Investment Platforms

Round-trip transactions aren’t confined to corporate books—they’re also prevalent in financial markets, particularly in trading platforms where the intent is often market manipulation. Red flags in this context include:

- Wash trades—simultaneous buy and sell orders with no real market exposure

- High-frequency trades with the same counterparty, creating the illusion of liquidity or demand

- Non-arms-length trades between affiliated parties designed to boost trading volume or prices

Such practices distort the true state of the market, leading to artificial price inflation and misleading trading data. Regulators are increasingly deploying algorithmic surveillance tools to monitor and detect suspicious trading behaviors.

Safeguards and Strategic Oversight

Combatting round-tripping requires a multi-layered defense strategy involving people, processes, and technology. We advocate the following approaches:

- Meticulous scrutiny of financial records—with particular attention to revenue consistency, receivables quality, and cash flow coherence

- Thorough due diligence procedures across vendor onboarding and intercompany transactions

- Benchmarking performance data against industry standards to identify deviations

- AI-based monitoring systems that learn transaction patterns and flag anomalies

- Cross-functional audit teams equipped with forensic accounting and legal expertise

The long-term solution lies in creating an organizational culture that prioritizes financial integrity and regulatory compliance over short-term performance metrics.

Conclusion: A Clear-Eyed Approach to Financial Integrity

Round-trip transactions, whether deployed to mislead shareholders, dodge taxes, or simulate business health, erode the very foundations of trust in financial systems. As the corporate and investment landscape grows more interconnected, the risk of circular transactions becomes more complex and globally scaled.

To counteract this, we must enforce rigorous oversight, foster cross-border regulatory cooperation, and equip institutions with forensic tools and ethical frameworks. Only by doing so can we uphold the credibility of financial reporting and maintain investor confidence in an era of increasing scrutiny and data transparency.