The question “How many Boeing 737 MAX jets have been delivered so far?” is no longer just a statistical curiosity. It has become a real-time barometer of industrial recovery, regulatory trust, airline fleet strategy, and global passenger demand. Every aircraft handed over is not simply a transaction—it is a data point in one of aviation’s most closely watched comeback stories.

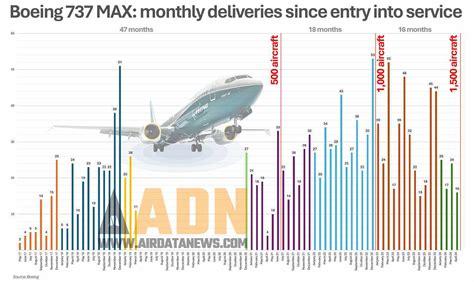

As of January 2026, Boeing has delivered 2,157 aircraft from the 737 MAX family. That figure marks a decisive transition from crisis-era backlog clearing to sustained, regulator-approved production output. For airlines scrambling to meet record passenger volumes while retiring aging narrowbodies, these deliveries are essential capacity injections. For Boeing, they represent restored cash flow, operational discipline, and a step toward reputational repair.

The number 2,157 is more than cumulative volume. It signifies the end of a prolonged storage period, the normalization of supply chains, and the beginning of a new production phase no longer dependent on clearing parked aircraft.

The 2,157-Aircraft Milestone: What It Really Means

Reaching 2,157 total deliveries required navigating years of groundings, regulatory overhaul, production pauses, and quality audits. During the global grounding period, dozens of completed aircraft accumulated at storage locations such as Moses Lake. For years, delivery totals were artificially boosted by pulling these aircraft from what industry insiders called the “shadow factory.”

By early 2026, that backlog has effectively been cleared. The final 737-8 and 737-9 units built prior to August 2025 have now been delivered. This marks a structural shift. Current delivery figures are no longer padded by stored inventory. Instead, they reflect real-time output from Boeing’s active production lines in Renton.

That distinction matters. A delivery number built on stored aircraft can mask production instability. A delivery number built on newly manufactured jets indicates industrial alignment with demand. The MAX program has now entered the latter phase.

In January 2026 alone, Boeing handed over 46 commercial aircraft, including 38 units of the 737 MAX, allowing it to temporarily outpace Airbus in narrowbody deliveries during that month. This momentum suggests that production stabilization efforts are taking hold.

Production Rate: The Engine Behind Delivery Growth

Deliveries are downstream of manufacturing rhythm. The Federal Aviation Administration currently authorizes Boeing to produce 42 737 MAX aircraft per month. Any move toward the company’s target of 52 aircraft per month by the end of 2026 depends entirely on meeting strict quality benchmarks.

The roadmap looks like this:

- Current authorized monthly rate: 42 aircraft

- Mid-2026 ramp-up target: 47 aircraft per month

- End-of-2026 goal: 52 aircraft per month

- Long-term ambition (2027–2028): 63 aircraft per month

This ramp-up is not automatic. The regulatory environment is zero tolerance. Any spike in manufacturing defects, “traveled work” (tasks completed out of sequence), or quality escapes could immediately halt further increases.

A critical operational shift supporting this ramp is Boeing’s reintegration of Spirit AeroSystems. By bringing key fuselage production closer under its direct oversight, Boeing aims to reduce workflow disruptions that previously led to delivery delays and costly rework.

The significance is simple: without production stability, delivery momentum collapses. Now that the storage buffer is gone, a one-week pause at Renton would immediately reflect in monthly delivery numbers.

Variant Breakdown: MAX 8 And MAX 9 Carry The Load

Although 2,157 deliveries sounds comprehensive, the number is heavily concentrated in two variants: the 737 MAX 8 and the 737 MAX 9. These aircraft form the backbone of current deliveries and airline fleet expansion plans.

The MAX 8 remains the dominant variant. It offers roughly 20% improved fuel efficiency compared to previous-generation 737NG aircraft, making it especially attractive to low-cost carriers expanding aggressively on international routes. The high-density MAX 8-200 configuration has gained traction among operators seeking maximum seat economics.

India’s Akasa Air, for example, received its 34th 737 MAX 8-200 in February 2026, marking its third delivery in under two months. Such rapid induction reflects the aircraft’s operational appeal.

However, two planned variants—the MAX 7 and MAX 10—have yet to be delivered commercially. Certification delays tied to engine anti-ice system modifications have pushed their entry into service into late 2026 or 2027.

Nearly 1,300 aircraft in Boeing’s backlog remain undeliverable until these variants receive final FAA approval. That creates a lopsided delivery profile: strong overall volume but zero output in two strategically important segments.

Certification Bottlenecks: The MAX 7 And MAX 10 Waiting Game

Airlines that bet heavily on the MAX 7 and MAX 10 now face constrained growth timelines.

Southwest Airlines expects MAX 7 certification around August 2026, but passenger service is not anticipated until early 2027 due to induction and pilot training requirements. United Airlines has adjusted its fleet plan, leaning on MAX 9 aircraft and leased Airbus A321neos to fill capacity gaps until the MAX 10 arrives in volume.

The MAX 10 is particularly critical. It is Boeing’s answer to the Airbus A321neo, which dominates the high-capacity, long-range single-aisle segment. Without MAX 10 certification, Boeing lacks a direct competitor in that space.

The technical issue delaying certification centers on the engine anti-ice system. Final validation testing is underway, but any unexpected performance anomaly could push approvals further into 2027.

The market is watching closely. Certification success would unlock a substantial portion of the 4,887-aircraft MAX backlog and materially accelerate future delivery totals.

Boeing Versus Airbus: Delivery Numbers In Context

While Boeing has delivered 2,157 MAX aircraft, Airbus has delivered 4,387 A320neo-family jets as of January 2026. The European manufacturer maintains a clear cumulative lead.

Interestingly, January 2026 saw Boeing temporarily outperform Airbus in narrowbody deliveries—38 MAX aircraft versus 15 A320neo-family jets that month. However, Airbus historically concentrates deliveries in end-of-year surges, including 136 jets in December 2025 alone.

The structural difference is strategic. Airbus maintains consistent high-volume output. Boeing is attempting to shift from erratic surges toward steady monthly production under regulatory scrutiny.

Airbus also retains dominance in the higher-capacity segment. The A321neo continues to command strong demand, accounting for most of Airbus’s narrowbody deliveries in early 2026.

Until the MAX 10 enters service, Boeing competes primarily with the MAX 8 and MAX 8-200, leaving a competitive gap in long-range, single-aisle routes.

Clearing The Shadow Factory: A Psychological Turning Point

For years, Boeing’s delivery numbers were tied to clearing parked aircraft from storage fields. Those images—rows of silent jets waiting for approval—became symbolic of the program’s struggles.

With the final stored aircraft delivered by early 2026, the MAX program has entered what industry observers call the “post-storage era.” Deliveries now reflect fresh production rather than backlog liquidation.

This shift carries psychological weight. Airlines no longer worry about inheriting long-stored aircraft requiring additional inspections. Regulators see stabilized quality processes. Investors see cash flow tied to current manufacturing rather than inventory clearance.

The 2,157-delivery figure therefore represents more than arithmetic. It marks the close of a recovery phase defined by mitigation and the start of a phase defined by sustainable output.

Delivery Pace And Cash Flow Stability

Each 737 MAX delivery translates into substantial revenue recognition. During grounding years, Boeing’s cash flow suffered from halted deliveries even as fixed costs continued.

With monthly output stabilizing at 42 aircraft, Boeing’s financial recovery aligns directly with delivery consistency. Maintaining that pace is essential. Unlike in previous years, there is no inventory cushion.

If supply chain disruptions re-emerge, if quality inspections slow output, or if regulatory audits pause line operations, delivery counts would immediately decline. The absence of stored aircraft eliminates any buffer.

This new reality increases operational pressure but also reflects maturity. The program now stands on its production integrity alone.

Airline Sentiment: From Safety Doubts To Logistics Planning

The narrative surrounding the MAX has evolved. Early debates focused on safety recertification. Today, airline executives concentrate on scheduling integration and delivery timing.

Ryanair’s Michael O’Leary, once sharply critical of Boeing’s leadership, recently praised the accelerated pace of MAX 8-200 deliveries. The airline projects carrying over 260 million passengers by 2027 if current induction rates continue.

Market analysts at S&P Global suggest that if Boeing maintains 42 aircraft per month without quality regressions, 2026 may be remembered as the year the program shifted from crisis containment to durable recovery.

That sentiment depends heavily on variant certification. The moment the MAX 7 and MAX 10 begin flowing through delivery channels, cumulative totals could accelerate significantly.

The Backlog: Nearly 5,000 Aircraft Waiting

Beyond the 2,157 delivered aircraft, Boeing holds a backlog of 4,887 MAX orders. This represents roughly a decade of production at current rates.

Backlog health signals sustained airline confidence in the platform. Despite its troubled history, carriers continue to view the MAX family as an essential component of fleet modernization.

Production wait times currently stretch close to ten years. Airbus maintains a similar timeline. In practical terms, airlines are securing delivery slots deep into the 2030s.

That long horizon underscores the importance of regulatory trust and quality control. A single systemic issue could ripple across thousands of pending aircraft.

What Happens Next?

The immediate trajectory depends on three variables: certification success, production ramp discipline, and supply chain stability.

If Boeing achieves its 52-aircraft-per-month goal by late 2026, annual deliveries could exceed 600 units. Combined with MAX 7 and MAX 10 certification, cumulative totals would rise sharply beyond the current 2,157 figure.

If ramp-up stalls, delivery growth will flatten. The absence of stored inventory means there is no fallback mechanism.

Early 2026 represents a hinge moment. The storage era has ended. The production era has begun. The question “How many Boeing 737 MAX jets have been delivered so far?” currently resolves to 2,157 aircraft—but the more meaningful inquiry is whether that number now grows through disciplined manufacturing rather than crisis recovery.

The answer will define not only Boeing’s narrowbody future, but the competitive balance of the global single-aisle market for the next decade.