The Boeing 787 Dreamliner was never meant to be just another widebody. It was conceived as a strategic pivot, a calculated departure from the industry’s obsession with sheer size. Instead of building the biggest aircraft in the sky, Boeing built one of the smartest. In just over fourteen years of commercial service, the 787 has transported more than a billion passengers, completed nearly five million flights, and accumulated over 2,000 orders from close to 90 customers worldwide. That is not incremental success. That is structural dominance.

For Airbus, the implications are profound. The world’s best-selling passenger widebody is not simply a commercial win for Boeing; it is a reshaping of long-haul economics, airline network planning, and passenger expectations. Every additional Dreamliner delivered reinforces a market narrative that Boeing owns the mid-size, long-range segment. In a duopoly industry where perception often drives purchasing momentum, that narrative matters.

The anxiety in Toulouse is not about a single aircraft program. It is about long-term positioning. The 787 has become the default answer for airlines seeking fuel efficiency, operational flexibility, and global range without the financial exposure of larger jets. When an aircraft becomes the industry’s safe bet, competitors face a far steeper climb.

The Rise Of The Boeing 787 Dreamliner: A Gamble That Paid Off

When Boeing launched the 787 program in the early 2000s, it was making a philosophical bet. The prevailing logic of long-haul aviation favored capacity growth through giants like the Boeing 747 and Airbus A380. Boeing countered with a different thesis: airlines did not need more seats; they needed more efficiency and more direct city pairs.

The Dreamliner entered service in 2011 after well-documented delays and technical turbulence, including high-profile battery issues that temporarily grounded the fleet. Skeptics predicted long-term reputational damage. Instead, once operational stability was achieved, the aircraft delivered exactly what airlines were promised—lower fuel burn, improved reliability, and flexible route economics.

Today, more than 1,250 Dreamliners are flying across the globe, with hundreds more on order. It became the first twin-aisle aircraft in history to surpass 2,000 sales. That milestone alone signals a transformation. Widebodies were once niche assets purchased cautiously. The 787 normalized them as growth engines.

Airlines from All Nippon Airways to United Airlines, from Qatar Airways to British Airways, embedded the aircraft deeply into their long-haul strategies. Leasing companies followed, amplifying the order pipeline. The result is a powerful feedback loop: high adoption builds confidence, which drives more adoption.

Efficiency That Rewrote Long-Haul Economics

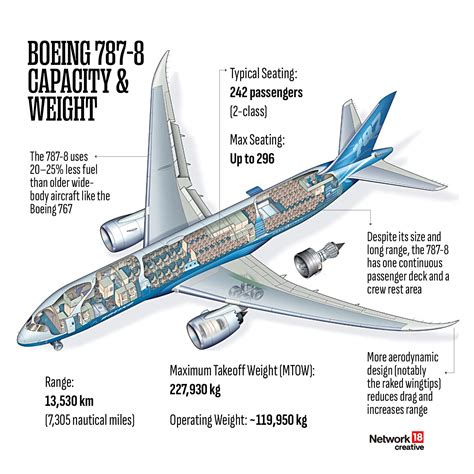

The Dreamliner’s dominance begins with physics and materials science. Approximately 50% of its primary structure is made from carbon-fiber-reinforced polymer composites. These materials are lighter than traditional aluminum and more resistant to corrosion and fatigue. Lighter structure means lower fuel burn. Lower fuel burn means lower operating costs. Aviation, at its core, is a math problem conducted at 35,000 feet.

Compared with older-generation widebodies, the 787 delivers roughly 20–25% lower fuel consumption. That margin is not incremental; it is transformative. For airlines operating ultra-long-haul sectors where fuel represents a substantial share of total operating cost, a double-digit efficiency gain can determine whether a route survives or fails.

The aircraft’s advanced aerodynamics, including raked wingtips and optimized wing flexibility, reduce drag. Its engines—either the General Electric GEnx or the Rolls-Royce Trent 1000—push high-bypass turbofan technology to new efficiency thresholds. High-bypass means a larger volume of air moves around the engine core rather than through combustion, improving fuel economy and lowering noise.

Passengers feel the difference too. Higher cabin humidity, larger electronically dimmable windows, and lower cabin altitude reduce fatigue. These comfort upgrades are not superficial marketing touches. They contribute to airline brand differentiation. When passengers prefer a particular aircraft type, airlines notice.

Airbus understands this dynamic well. The challenge is that the A330neo, its closest competitor to the 787, does not enjoy the same widespread perception of being revolutionary. It is seen as evolutionary—a refinement of a proven platform rather than a structural reinvention.

Opening New Routes And Breaking The Hub Model

Perhaps the Dreamliner’s most consequential achievement is how it reshaped route planning. With a range of roughly 7,500 nautical miles, depending on variant, the 787 unlocked what industry planners call “long and thin” markets. These are routes too distant for narrowbodies but too low in demand to justify larger widebodies.

Instead of funneling passengers through mega-hubs, airlines began connecting secondary cities directly. Tokyo to San Jose. Perth to London. Denver to Tokyo. These routes would have struggled under older widebody economics. The 787 made them viable.

This shift carries strategic consequences. Hub-and-spoke systems concentrate power in major airports. Point-to-point long-haul service distributes it. Airlines can differentiate themselves by offering direct connectivity where competitors require connections. Premium travelers, especially corporate clients, gravitate toward nonstop convenience.

Airbus’ A350 has excelled in the larger long-range segment, competing more directly with Boeing’s forthcoming 777X. But the mid-size widebody sweet spot—large enough for intercontinental range, small enough to maintain high load factors—has been where the 787 thrives. Airbus risks being squeezed between categories.

Airbus On The Defensive In The Mid-Size Widebody Segment

The Airbus A330-900neo was designed to counter the Dreamliner’s appeal. It offers updated engines, improved aerodynamics, and competitive operating economics. On paper, it stands close in seating capacity and range to the 787-9. In practice, however, sales momentum has tilted heavily toward Boeing.

Market psychology plays a powerful role. When airlines and lessors see a program surpass 2,000 orders, they interpret it as validated technology. Residual value forecasts strengthen. Financing becomes easier. The aircraft transforms into a low-risk asset.

Airbus faces a structural dilemma. The A350 is widely praised and commercially successful in its own right, but it operates primarily in a larger capacity bracket. It does not directly displace the 787 in most fleet-planning scenarios. Meanwhile, the A330neo competes head-to-head yet lacks equivalent sales traction.

This positioning gap is subtle but significant. In aviation, segments matter. If one manufacturer dominates a specific category for a decade or more, airline fleet commonality trends begin to entrench that dominance. Pilots are trained on it. Maintenance systems adapt to it. Spare parts ecosystems mature around it. Switching costs increase.

The concern for Airbus is not simply losing orders today. It is losing structural influence over tomorrow’s fleet architectures.

Cracks In Boeing’s Armor: Opportunities For Airbus

No aircraft program is invulnerable. The 787 has faced production pauses, quality-control scrutiny, and supply-chain disruptions. Deliveries have occasionally slowed, frustrating airlines awaiting capacity expansion. Regulatory oversight has intensified.

These episodes matter. Airlines value reliability not only in operations but also in manufacturer partnerships. When delivery schedules slip, route planning suffers. Airbus has attempted to position itself as the steadier alternative during such disruptions.

Sustainability introduces another competitive variable. Governments and regulators are tightening carbon targets. Sustainable Aviation Fuel (SAF) adoption is increasing, but long-term decarbonization may require deeper technological shifts—hybridization, hydrogen experimentation, radical aerodynamic redesigns.

If Airbus were to launch a next-generation mid-size widebody incorporating step-change efficiency gains beyond incremental upgrades, it could potentially disrupt the 787’s long tenure. However, launching a clean-sheet program demands enormous capital, supplier alignment, and risk tolerance. The memory of costly development cycles is fresh in both Seattle and Toulouse.

Another subtle vulnerability lies in lifecycle perception. The 787 program began development more than two decades ago. While still technologically advanced, aviation innovation does not pause. Materials science, digital manufacturing, and propulsion research continue to evolve. At some point, the industry will expect a successor.

Should Airbus Be Worried About The Boeing 787’s Dominance?

Strategically, yes—but not defensively. The Dreamliner’s success signals a durable market shift toward efficient, flexible widebodies optimized for direct connectivity. Airbus must decide whether to counter within the existing framework or leapfrog it entirely.

The A350 provides Airbus with strength in higher-capacity long-haul operations, and early traction against the delayed 777X strengthens that position. Yet the absence of a runaway mid-size widebody success story equivalent to the 787 leaves a competitive imbalance.

The aviation duopoly thrives on alternating cycles of innovation. One manufacturer advances; the other recalibrates and responds. The 787 represents Boeing’s decisive move in the early 21st century widebody chess game. Airbus now faces the strategic question of whether incremental updates suffice or whether a bold new aircraft must redefine the segment once again.

For now, the numbers speak loudly. Over a billion passengers. Nearly five million flights. More than 2,000 orders. The Boeing 787 Dreamliner is not merely the world’s best-selling passenger widebody of all time—it is a case study in how engineering philosophy, economic timing, and market psychology can converge into sustained dominance.

Airbus is not cornered, but it is challenged. And in aviation, sustained challenge is the engine of the next breakthrough.

")