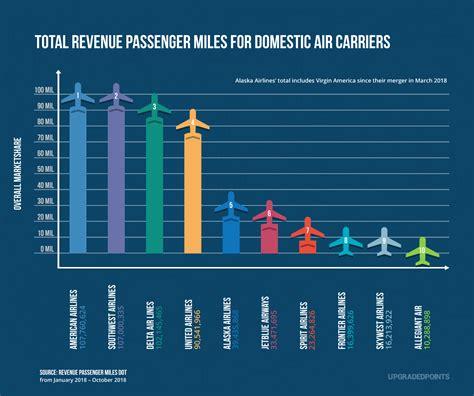

Delta Air Lines, Southwest, American Airlines, Frontier, and other major U.S. carriers are grappling with a sobering financial reality in the first quarter of 2025. After enjoying a string of profitable quarters throughout 2024, the industry has posted a collective $225 million after-tax net loss in Q1, signaling a potentially turbulent year ahead. The losses, though smaller than Q1 2024’s $1.7 billion setback, mark a sharp reversal from the $2.4 billion profit recorded just one quarter earlier.

This downturn reflects deeper structural weaknesses that have begun to resurface: shrinking domestic travel demand, a steep drop in international arrivals, and the weight of economic anxiety on consumer behavior. The optimism that characterized the aviation rebound post-pandemic is now replaced with cautious restraint as carriers scramble to adapt.

Economic Slowdown Undermines Consumer Confidence and Travel Bookings

At the core of the downturn is the weakening of U.S. consumer buying power. According to data from the Federal Reserve Bank of St. Louis, real disposable income dropped to $17,978 as of April 2025, down sharply from the pandemic-era high of $20,445 in March 2021. This erosion in income has had a cascading impact on travel decisions, with airfare—often seen as a discretionary spend—among the first to be cut from household budgets.

Supporting this, a Bank of America report in May cited softened spending on airline tickets, lodging, and tourism activities. This decline in consumer-driven travel is particularly worrisome for low-cost carriers like Southwest and Frontier, which rely heavily on volume and price-sensitive travelers to drive margins.

Airline executives have taken note. American Airlines announced a $473 million Q1 loss, while Alaska Air Group posted a $166 million deficit, both scrapping full-year forecasts as volatility clouded visibility. Their moves reflect broader industry caution in a year that’s no longer trending upward.

Domestic and International Travel—Both Under Pressure

The downturn isn’t isolated to international routes. Domestic operations, traditionally the industry’s bedrock, also fell into the red on a pre-tax basis. Analysts attribute the contraction to a dual threat: reduced vacation demand and weaker corporate travel bookings.

The situation is no better abroad. The World Travel & Tourism Council (WTTC) estimates that the U.S. could lose $12.5 billion in international visitor spending in 2025—a jaw-dropping 22.5% decline from previous highs. Travel from key markets such as the United Kingdom (-15%), Germany (-28%), and South Korea (-15%) has plummeted.

These markets had been instrumental in supporting U.S. tourism recovery post-pandemic. Their absence is being acutely felt—not just by airlines, but by hotel operators, restaurant chains, and regional economies reliant on tourism dollars. International traveler confidence, rattled by fluctuating visa policies, geopolitical tensions, and inflation in originating countries, has yet to return to pre-2020 norms.

Government and Corporate Travel Contracts Decline Further

The decline in government and corporate travel compounds the financial woes. JP Morgan‘s aviation analysts noted a measurable dip in federal travel spending, a vital stabilizer for many carriers. Government contracts, while smaller in volume, are critical in ensuring consistent seat sales during economic downturns. Their decline represents not only a loss in revenue but in stability.

Meanwhile, the return-to-office slowdown and ongoing hybrid work models are undermining corporate travel recovery. Pre-2020, business travelers represented some of the most lucrative customers for legacy carriers. Today, many companies continue to impose travel restrictions or lean on virtual alternatives.

With these segments weakening in unison, airline balance sheets are starting to crack.

Aviation Stocks React as Carriers Revise Guidance

As losses mounted, U.S. airline stocks saw immediate impact. Multiple airlines, including United Airlines, JetBlue, and Spirit, revised their 2025 earnings forecasts downward. Historically, airline equities experience up to 40% drawdowns ahead of economic recessions, with the Dow Jones U.S. Airlines Index already showing signs of strain.

However, some analysts note that aviation stocks often recover faster than broader indices once a rebound begins, pointing to the need for longer-term patience and strategic realignment.

Carriers are responding with cost-cutting measures, capacity adjustments, and delayed fleet expansions. Boeing and Airbus have also reported a softening in new orders from U.S. clients, with some deliveries being postponed to 2026 and beyond.

Seasonal Travel and the Summer Outlook

Despite the dire Q1 results, there is some hope on the horizon. The American Automobile Association (AAA) projects that 5.84 million Americans will travel by air over the Fourth of July holiday in 2025—a 1.4% increase over last year, and a potential record for the holiday.

Such spikes are encouraging, but analysts caution that seasonal travel peaks cannot compensate for sustained declines across the year. Airlines are closely watching the Labor Day and Thanksgiving periods, hoping to capture last-minute revenue boosts.

Airlines are also introducing flash sales, fuel hedging strategies, and partnership promotions with hotel chains to stimulate demand. These tactical plays, however, are no substitute for the structural changes needed to weather the rest of the year.

Policy Uncertainty and the Need for Federal Leadership

While the airlines bear much of the financial brunt, the broader U.S. travel ecosystem is feeling the pain—and some argue that it’s time for federal leadership to step up.

The WTTC and other industry stakeholders are calling on Congress and the White House to pass more traveler-friendly policies, including improved visa processing times, investment in airport infrastructure, and a renewed global marketing push to attract international visitors.

Without these interventions, the U.S. risks falling further behind other global tourism powerhouses that have already returned to or exceeded their pre-pandemic visitor numbers.

Airlines at a Crossroads: Pivot or Perish?

What comes next for the U.S. airline industry remains uncertain. The $225 million Q1 loss could either serve as a wake-up call or the beginning of a prolonged crisis. Industry leaders must now balance immediate tactical responses—cutting costs, optimizing schedules, and managing investor expectations—with long-term strategic recalibrations.

That includes exploring sustainable fuel options, diversifying route structures, and embracing digital transformation to reduce operational inefficiencies. The future of air travel may no longer be just about planes in the sky—it’s about creating a more resilient and adaptive system ready to face economic shocks.

The engines are still running, and the runway is long. But for now, America’s airline industry is flying through fog, trying to navigate toward clearer skies.