Visa has announced a new rewards integration that allows eligible Visa cash back credit card rewards to be deposited directly into Trump Accounts, a recently introduced savings vehicle tied to U.S. tax policy for children. The move blends mainstream credit card infrastructure with a politically branded financial product, immediately drawing attention across both the payments industry and the broader financial policy landscape.

The announcement was made by former President Donald Trump, who credited Visa with building a dedicated platform to enable the feature. According to the statement, Visa cardholders will soon be able to redirect earned cash back into Trump Accounts rather than redeeming rewards as statement credits, bank deposits, or gift cards. The initiative positions Visa as the first major card network to formally support this specific account structure.

The timing of the announcement is notable. Consumer cash back rewards have become one of the most competitive battlegrounds in the U.S. credit card market, while political branding in financial products remains rare and controversial. Visa’s decision signals a willingness to support alternative redemption pathways that align with policy-driven savings programs, even when the branding itself is polarizing.

How the Visa–Trump Accounts Integration Works

Under the new platform, Visa cardmembers will be given the option to allocate their accumulated cash back rewards directly into Trump Accounts through participating issuers. From a technical standpoint, this is an extension of Visa’s existing rewards infrastructure, which already supports deposits into checking accounts, brokerage platforms, and external savings products.

The difference lies in the destination and framing. Trump Accounts are positioned not as personal spending vehicles, but as long-term savings accounts intended for children. By integrating rewards deposits, Visa is effectively enabling parents and guardians to convert everyday spending into structured savings contributions without requiring additional out-of-pocket transfers.

Visa has not disclosed which issuing banks will support the feature at launch, nor whether all cash back cards will be eligible. Historically, such integrations roll out selectively, often starting with co-branded or premium products before broader adoption.

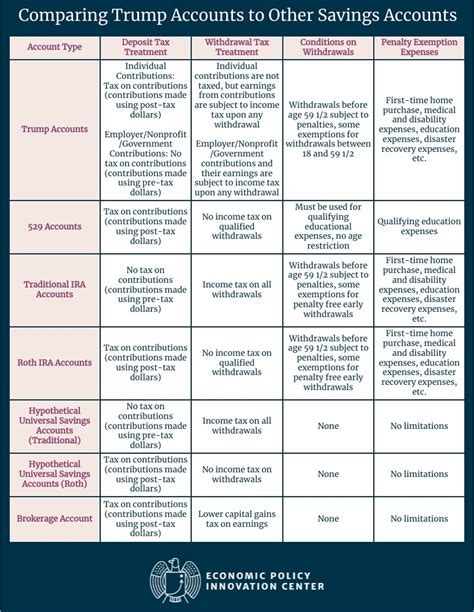

What Exactly Are Trump Accounts?

Despite the branding, Trump Accounts are not personal accounts tied to Donald Trump, nor are they a private banking product. They are a newly authorized type of individual retirement-style savings account for children, established under the Working Families Tax Cuts framework.

According to IRS guidance, Trump Accounts can be opened for children under the age of 18 who possess a valid Social Security number. A pilot program includes a $1,000 government contribution for qualifying children born between January 1, 2025, and December 31, 2028, provided they meet citizenship requirements.

Functionally, the accounts resemble other long-term custodial savings vehicles. Funds are intended to grow over time, with contributions coming from parents, guardians, or other authorized individuals. Visa’s rewards integration simply adds another funding source, converting consumer credit card spending into incremental savings.

Why Visa’s Move Matters in the Credit Card Industry

From an industry perspective, the announcement reflects a broader shift toward purpose-driven rewards redemption. Cash back has historically been flexible but generic. Allowing rewards to flow directly into child-focused savings accounts reframes cash back as a financial planning tool rather than discretionary income.

This approach is not entirely new. Some niche credit cards already market themselves around funding education or savings goals. What sets this apart is Visa’s scale. As the world’s largest card network, Visa’s endorsement gives Trump Accounts instant visibility and legitimacy within mainstream consumer finance.

There is also a strategic undercurrent. Trump has previously floated proposals to cap credit card interest rates at 10%, accompanied by warnings of legal consequences for non-compliant issuers. While no such cap has materialized, Visa’s cooperation on Trump Accounts may be viewed as a gesture of alignment with broader consumer-facing initiatives tied to his policy agenda.

Potential Impact and Public Reaction

Reactions are likely to be mixed. Supporters may see the integration as a practical way to encourage early savings for children using money that might otherwise be casually spent. Critics may focus on the politicization of financial products and question whether branding alone could deter adoption among certain consumers.

From a purely functional standpoint, the feature does not create a capability that was previously impossible. Consumers could already redeem cash back to bank accounts and manually transfer funds. The value lies in convenience, visibility, and intent, lowering friction and framing rewards as long-term investments.

Bottom Line

Visa’s decision to allow cash back credit card rewards to be deposited into Trump Accounts introduces a new, highly visible redemption option tied to child-focused savings and federal tax policy. While the branding ensures controversy, the underlying concept aligns with broader trends in rewards innovation and financial planning. Whether it gains meaningful adoption or remains a symbolic gesture, the move underscores how even routine credit card perks are becoming tools in larger economic and political narratives.