Modern aviation has long relied on a delicate, largely invisible framework: the expectation that airspace, once granted, remains predictable and open. For decades, airlines meticulously optimized their route networks around stable overflight rights, balancing efficiency, fuel consumption, and operational precision. Each shortcut in the sky, every direct corridor, was the result of complex planning designed to shave hours off long-haul flights while minimizing costs. Yet, in recent years, this predictable architecture has been steadily undermined by geopolitical tensions, most notably airspace closures over Russia, Ukraine, and more recently, Iran. The effects of these closures are neither uniform nor instantaneous—they ripple quietly through the global network, forcing airlines to rethink strategies, altering competition, and subtly reordering the geography of connectivity.

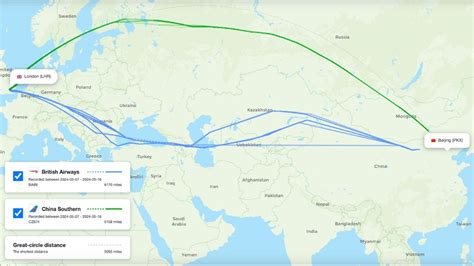

The sudden closure of Russian airspace to Western carriers following the invasion of Ukraine was a seismic disruption. Russia’s skies, once a major conduit for flights between Europe and Asia, vanished almost overnight from the operational map for carriers like Finnair and LOT Polish Airlines. Helsinki’s strategic advantage as a hub connecting Europe to Asia was instantly eroded, lengthening flights, increasing fuel burn, and forcing airlines to restructure schedules and fleet usage. Meanwhile, airlines with continued access, particularly Chinese and some Middle Eastern carriers, suddenly gained a competitive edge, able to operate shorter routes at lower operational costs. This asymmetry created a new, uneven playing field, highlighting how critical overflight rights had become as a core competitive asset rather than a mere logistical detail.

While Russia dominated headlines, Ukraine’s airspace closures added another, less visible layer of disruption. Though not a central corridor like Russia, Ukrainian skies played a crucial supporting role in European routing, especially for flights connecting Western Europe, the Middle East, and parts of Asia. With Ukrainian airspace off-limits, airlines were forced to condense flight paths into narrower channels over Romania, Hungary, and Turkey. This rerouting introduced congestion, heightened strain on regional air traffic control systems, and eliminated many alternative options for handling weather delays or operational disruptions. Hubs such as London Heathrow (LHR), Frankfurt (FRA), and Amsterdam Schiphol (AMS) had to adapt schedules, adjust connection banks, and reallocate aircraft, creating knock-on effects that cascaded through the broader network.

In the Middle East, the closure of Iranian airspace triggered a sharper, more volatile response. Unlike the gradual adjustments in Europe, airlines faced immediate operational crises as significant portions of airspace became inaccessible due to escalating regional tensions. The Middle East serves as one of the planet’s most vital crossroads, linking Europe, Asia, and Africa. Any disruption here reverberates across the entire system, affecting global connectivity. Airlines had to reroute quickly, in some cases suspending services or taking longer, less efficient paths, dramatically increasing fuel costs and operational uncertainty. For carriers like Emirates and Qatar Airways, the closure demanded rapid reassessment of network planning, while European carriers were forced into longer, costlier flight paths that reshaped competitive dynamics.

The economic implications of these detours are immediate and stark. Flight distances have ballooned by hundreds, sometimes thousands, of miles. Fuel consumption—the single largest variable cost for airlines—rises accordingly, with the knock-on effects extending to crew scheduling and aircraft utilization. Longer flights tie planes in the air for extended periods, reducing daily flight rotations and increasing labor costs due to longer duty times. Payload restrictions are sometimes imposed to accommodate extra fuel, limiting passenger numbers or cargo capacity. Airlines have responded with a combination of fare adjustments, route reductions, and selective market withdrawals. For long-haul Europe-Asia services, these shifts have made tickets both more expensive and less predictable, fundamentally altering the economic calculus for travelers and carriers alike.

Beyond economics, airspace closures have injected new operational complexity into daily airline management. Flight planning has become a dynamic, real-time endeavor, requiring constant vigilance over geopolitical developments, airspace regulations, and safety advisories. Pilots, cabin crew, and dispatch teams must coordinate across multiple air traffic jurisdictions to ensure compliance while minimizing delays. Scheduling becomes a delicate balance; extended flights must respect crew duty limits, while fleet deployment must maintain service reliability without inflating costs. The broader aviation system has felt these pressures as well—alternative corridors grow congested, risk of delays rises, and system-wide resilience is tested daily. Airports and air traffic control authorities must constantly adjust to traffic surges in formerly secondary routes, making once-stable networks more fluid and unpredictable.

Network realignments have produced winners and losers in unexpected ways. Finnair, heavily impacted by lost access to Russian airspace, has shifted strategy, bolstering intra-European connectivity and exploring non-traditional long-haul destinations beyond Asia. This adaptation demonstrates how carriers must balance historical advantages with operational realities. Meanwhile, airlines with unobstructed access to critical regions, particularly in Asia and the Middle East, have expanded market share on routes where competitors face limitations, consolidating influence and profitability. Secondary hubs have also emerged as beneficiaries. Passengers, seeking efficiency or safety, increasingly choose alternative routing options, inadvertently redistributing global traffic and creating new opportunities in previously marginal airports.

Iran’s closures, coupled with ongoing US-Iran tensions, have particularly underscored the fragility of global routing. Gulf carriers now incur some of the highest per-hour costs in aviation when circumventing Iranian airspace, highlighting the financial pressures imposed by geopolitical constraints. The rapid adaptation required has forced airlines to re-evaluate everything from fuel management and flight planning software to emergency contingency procedures. Such volatility reinforces the idea that modern airspace closures are not isolated incidents but catalysts for broader structural change within aviation networks.

The geopolitical reshuffling extends further into fleet and hub strategy. Carriers have been forced to rethink the allocation of long-range aircraft, prioritizing flexibility over traditional routing efficiency. For instance, widebody fleets capable of ultra-long-haul operations have become strategic assets, as they allow airlines to bypass restricted airspace without compromising non-stop service. Airlines also face new considerations in crew deployment; multi-sector rotations must account for variable flight durations and legal duty limits, a challenge amplified by frequent reroutes. The operational ripple effects influence maintenance schedules, turnaround times, and even airport slot utilization, creating a web of interconnected adjustments that redefine aviation operations at every level.

The cascading effect of these closures also reshapes the competitive landscape. Airlines operating within unaffected corridors gain the ability to offer shorter, faster, and more reliable services, sometimes at lower prices, while those constrained by closures face higher costs and longer flight times. This has reinforced the importance of geopolitical positioning as a strategic asset, sometimes outweighing traditional factors like fleet size or brand reputation. Observers now recognize that airspace access can determine market leadership on intercontinental routes, particularly in Europe-Asia and Europe-Middle East connections, where traditional competitive advantages are suddenly insufficient to counter the operational impact of closures.

Historically, airlines relied on redundancy in airspace options to manage risk. Detours due to weather, technical delays, or congestion were easily absorbed because multiple viable routes existed. Today, closures reduce redundancy to a fraction of former levels, forcing reliance on narrower corridors and amplifying the consequences of disruptions. A single adverse event in these compressed channels now carries greater operational risk, affecting flight punctuality, connection reliability, and passenger satisfaction. Air traffic control authorities must manage higher traffic densities with fewer alternatives, increasing the potential for system-wide ripple effects across continents.

The implications for air cargo are equally pronounced. Freight carriers, particularly those operating time-sensitive shipments between Europe and Asia, face higher costs and slower delivery times due to extended routing. The financial burden can translate into higher prices for shippers and downstream industries, emphasizing that airspace closures affect not only passengers but also global supply chains. Some carriers have responded by rerouting cargo through less congested secondary hubs, creating new logistics patterns and redistributing freight flows in ways that were previously unanticipated.

The cumulative effect of modern airspace closures is a quieter, more subtle restructuring of global aviation than dramatic crises of the past. Unlike airline bankruptcies or airport strikes, these disruptions do not create instant headlines; instead, they evolve over months or years, altering economic, operational, and competitive landscapes in a slow, persistent manner. Observers note that airlines are not merely reacting—they are evolving. The industry has entered an era where adaptability and strategic foresight, rather than operational inertia, define success. Airlines capable of rapidly reallocating resources, recalibrating networks, and leveraging access to unrestricted airspace are emerging stronger, while others confront the real cost of vulnerability.

In essence, airspace closures have transformed the global aviation map into a more fluid, politically sensitive network. Traditional hubs must contend with rerouted traffic, longer flight times, and operational uncertainty, while opportunistic carriers exploit new corridors and secondary airports to gain competitive advantage. This quiet reshuffling reinforces the idea that in modern aviation, access to the sky is as vital as access to the ground. Airlines are learning, often the hard way, that geopolitical developments can be as consequential as market demand in shaping operational strategy.

Looking forward, the industry faces a landscape where the stability of airspace can no longer be taken for granted. Long-term planning must incorporate geopolitical risk assessments, flexible routing strategies, and adaptable fleet management policies. Governments and regulatory authorities also play a more visible role, as their decisions on overflight rights, airspace restrictions, and safety advisories directly influence market competition and operational efficiency. Airlines that invest in predictive analytics, scenario planning, and resilient operational frameworks are likely to outperform peers, while those anchored to historical routing patterns risk being increasingly marginalized.

In conclusion, modern airspace closures have quietly but decisively reshaped global aviation. From economic pressures on long-haul carriers to the strategic advantage of access-controlled airspace, the ramifications are multi-layered and enduring. The industry is now navigating a complex mosaic of restrictions, detours, and emergent corridors, requiring a level of strategic agility unseen in previous decades. For travelers, the effects manifest in longer journeys, higher fares, and shifting hub preferences; for airlines, they dictate fleet deployment, network realignment, and competitive positioning. The skies are no longer a stable, predictable environment—they are a geopolitical chessboard, where access, foresight, and adaptability determine winners and losers in the quiet yet profound reshaping of global aviation.

Joins Abu Dhabi (AUH), Doha (DOH), Riyadh (RUH), Amman (AMM), Beirut (BEY), and Sharjah (SHJ) Airports in Significant Disruptions Amid Regional Airspace Closures")