The modern aviation industry is built on precision timing. Aircraft deliveries, maintenance cycles, engine overhauls, and fleet expansions all move in synchronized rhythms measured in months and years. When that timing breaks, the consequences ripple globally. Today, airlines are confronting a disruption so severe that it is reshaping fleet economics: brand-new aircraft are being dismantled—not because they are obsolete, but because their engines are more valuable than the planes themselves.

This phenomenon is not symbolic exaggeration. It is a direct response to supply chain paralysis, engine shortages, and a maintenance backlog that has transformed spare parts into some of the most coveted assets in commercial aviation.

Supply Chain Disruption Becomes Aviation’s Permanent Operating Environment

What began as a pandemic-era manufacturing slowdown has evolved into a structural bottleneck. Airlines, lessors, and maintenance providers now operate in a world where component lead times stretch beyond a year. Before global disruptions, parts orders that once took months now linger in production queues indefinitely.

The implications are operational as much as financial. Aircraft cannot fly without certified components, and modern jets depend on intricate global supplier networks. A delay in turbine disks, avionics modules, or composite structures can ground entire fleets.

Demand has surged faster than production recovery. Passenger traffic rebounded sharply, forcing airlines to reactivate aircraft and accelerate maintenance schedules. Simultaneously, manufacturers ramped up output—but not fast enough to match the surge. The imbalance created a paradox: airlines need more aircraft in the sky, yet lack the parts to keep them there.

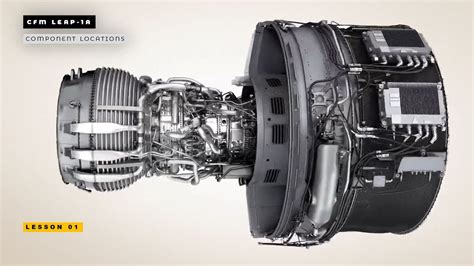

Engine Manufacturers Struggle to Match “Unimaginable” Demand

Few sectors feel the strain more acutely than engine production. Companies like CFM International have increased output since the pandemic, but airline and leasing demand has outpaced every forecast.

Jet engines are among the most complex machines ever mass-produced. Each unit contains tens of thousands of precision components operating under extreme heat and pressure. Scaling production is not as simple as adding factory shifts; it requires metallurgy capacity, supplier certification, and regulatory oversight.

The result is a sustained shortage of serviceable engines—especially next-generation models designed for fuel efficiency.

Pratt & Whitney’s GTF Crisis Intensifies the Shortage

If demand pressure lit the fuse, reliability issues poured fuel on the fire. Pratt & Whitney’s PW1000G Geared Turbofan (GTF) engines, widely used on Airbus A320neo and A321neo aircraft, have faced persistent manufacturing defects linked to contaminated powdered metal in critical turbine components.

The flaw can cause microscopic cracking, forcing premature inspections and removals. Regulators mandated widespread engine checks, grounding hundreds of aircraft globally.

By late 2025, more than 800 jets powered by PW1000G-family engines were grounded or stored—roughly a third of the global fleet using those powerplants. Aircraft that should have been revenue generators became stationary assets overnight.

Grounded planes created a vacuum in the parts ecosystem. Airlines needed replacement engines immediately, but production lines could not keep pace. That scarcity birthed a radical solution: cannibalization.

When Aircraft Become Spare Parts Warehouses

Aircraft cannibalization—the practice of removing usable components from one plane to keep others flying—is not new. Airlines have done it for decades with aging fleets. What is unprecedented is the age of the donor aircraft.

Instead of dismantling 20-year-old jets nearing retirement, companies are parting out aircraft barely six years old.

From a technical standpoint, these airframes are in their prime. Narrowbody jets like the A320neo family are designed for service lives exceeding 20–25 years. Structurally, they have decades of flight cycles ahead.

Economically, however, the equation has flipped.

Why the Parts Are Worth More Than the Plane

The financial logic is stark. A new Airbus A321neo carries a value exceeding $100 million at delivery. After several years in service, depreciation reduces its market value significantly—recent estimates place a six-year-old example near $42 million.

But the engines alone tell a different story.

An upgraded PW1100G engine can command more than $22 million on the secondary market. Since each aircraft has two engines, their combined standalone value can rival—or exceed—the worth of the entire jet.

Add other high-value components:

- Advanced avionics suites

- Flight control computers

- Landing gear assemblies

- Auxiliary power units

- Cabin electronics

Parted out, total recoverable value can surpass $55 million—far above the aircraft’s resale price as a complete unit.

Leasing Economics Accelerate the Cannibalization Trend

The profitability gap widens further in leasing markets. A six-year-old A321neo might generate roughly $350,000 per month in lease revenue.

Individually leased engines, however, can bring in around $200,000 per month each. Two engines alone can outperform the aircraft’s total leasing return.

For lessors managing portfolios worth billions, the math becomes irresistible. Selling or leasing engines separately maximizes yield while helping airlines solve urgent operational shortages.

The aircraft itself becomes secondary—a chassis whose most valuable organs have been extracted.

Real-World Cases: Young Aircraft Sent to the Scrapyard

The trend is no longer theoretical. Multiple A320neo-family aircraft have already been dismantled for parts, including high-profile cases involving nearly new jets.

Two IndiGo A321neos, just six years old, were sold specifically for teardown. Their remaining service life was sacrificed to feed the global spare-parts ecosystem.

Industry teardown specialists report a steady pipeline of similar aircraft entering disassembly facilities. At least 19 A320neo-family jets had been parted out by the end of last year, with more expected through 2026.

This is not driven by accidents or structural fatigue. It is driven purely by market demand for engines and components.

Airline Bankruptcies Add Fuel to the Parts Pipeline

Financial instability among carriers is accelerating supply. Airlines undergoing restructuring often shrink fleets rapidly, returning aircraft to lessors or storage facilities.

One of the most prominent examples is Spirit Airlines, which entered Chapter 11 restructuring proceedings for the second time in under a year. The airline moved aggressively to reduce fleet size, rejecting new aircraft deliveries and terminating dozens of leases.

Dozens of relatively young A320neo-family jets were placed into storage, including many relocated to long-term desert facilities such as Arizona’s Pinal County Airport.

Stored aircraft face uncertain futures. Some will find new operators, but others will likely be dismantled—particularly if their engines are in high demand.

The Rise of the “Cannibalization Economy”

This environment has created what industry insiders now call a cannibalization economy—a secondary market where dismantling aircraft is not a last resort but a strategic business model.

Teardown firms, maintenance providers, and leasing companies collaborate to extract, refurbish, certify, and resell components. Engines receive priority, but even cabin interiors and structural elements hold resale value.

The process is highly engineered:

- Aircraft arrive at specialized facilities.

- Technicians remove engines first.

- High-value avionics and electronics follow.

- Structural components are cataloged and stored.

- Remaining fuselage sections are recycled or scrapped.

Every part reenters the supply chain, often returning aircraft to service elsewhere.

Geopolitics and Manufacturing Complexity Deepen the Crisis

Supply constraints are not purely industrial—they are geopolitical. Aerospace manufacturing spans continents. Titanium may come from one region, semiconductor chips from another, and precision castings from yet another.

Trade tensions, export controls, and regional conflicts have complicated procurement flows. Even when factories are operational, logistics bottlenecks delay delivery.

Certification requirements compound the delay. Aviation regulators demand rigorous testing and traceability for every component. Substituting suppliers is neither quick nor simple.

Thus, shortages persist even as production lines attempt expansion.

What This Means for Fleet Strategy and Aircraft Longevity

Traditionally, airlines evaluated aircraft retirement based on age, fuel burn, and maintenance cost. Today, a new variable dominates: parts liquidity.

If an aircraft’s engines are scarce enough, dismantling it early can be financially rational—even if the airframe is mechanically sound.

This reframes aircraft ownership. Jets are no longer single revenue assets but modular collections of tradable components. Engines, landing gear, and avionics each have independent market cycles.

Fleet planners must now consider teardown value alongside operating economics when acquiring aircraft.

A Temporary Distortion or a Structural Shift?

Whether this trend endures depends on three variables:

- Engine production recovery

- Resolution of manufacturing defects

- Stabilization of global supply chains

If engine output accelerates and reliability issues are resolved, spare-parts scarcity will ease. Aircraft teardown rates would likely decline.

However, if demand continues outpacing supply, cannibalization may remain a fixture of aviation economics.

The industry has crossed a psychological threshold. It has proven willing to sacrifice young aircraft to sustain operational fleets.

The New Reality of Aircraft Value

Aviation has always been capital-intensive, but the engine crisis has exposed just how asymmetric aircraft value can be. The most technologically advanced jets in the sky are only as useful as the engines that power them.

When those engines become scarce, the hierarchy of value inverts. Airframes become accessories. Powerplants become currency.

That inversion explains the surreal image now appearing at teardown facilities worldwide: gleaming, modern aircraft—barely broken in—systematically dismantled to keep the rest of the world flying.

In an industry defined by engineering longevity, economics has emerged as the ultimate retirement clock.