The Airbus A321neo was supposed to represent the future of narrowbody aviation. Designed with advanced aerodynamics, lower fuel consumption, and next-generation propulsion systems, the aircraft quickly became one of the most desirable airliners ever produced. Airlines around the world placed massive orders, attracted by promises of lower operating costs, improved environmental performance, and the ability to serve both short- and medium-haul routes with exceptional efficiency.

Yet across parts of the aviation industry, a highly unusual trend has emerged. Some relatively young Airbus A321neos are being dismantled for spare parts despite being only a few years old. In an industry where modern aircraft are expected to remain productive for decades, seeing advanced airliners stripped of engines, avionics, landing gear, and other critical systems is startling.

The reason is not weak travel demand, declining profitability, or a flaw in the Airbus airframe itself. Instead, the phenomenon is largely driven by one of the most significant engine crises commercial aviation has faced in recent years: the shortage of Pratt & Whitney Geared Turbofan engines.

The situation has created a market distortion so severe that, in some cases, the components installed on an Airbus A321neo are worth more than the aircraft operating as a complete unit.

For airlines, lessors, investors, and maintenance providers, this unexpected reality is reshaping the economics of modern aviation.

After years of record aircraft demand and aggressive fleet expansion plans, few industry observers anticipated that some of the world’s most efficient passenger jets would become valuable sources of spare parts rather than revenue-generating assets.

The Unexpected Scene Unfolding at Aircraft Storage Facilities

One of the most visible examples of this trend can be found at Castellón Airport in eastern Spain. Traditionally known more for aircraft storage and maintenance activity than commercial passenger traffic, the facility has become a focal point for aircraft teardown operations involving relatively young Airbus A320neo-family aircraft.

Walking through the storage areas reveals a sight rarely associated with modern commercial aviation. Aircraft that should still be carrying passengers across Europe, North America, and Asia are instead being carefully dismantled by technicians.

Rather than scrapping aircraft indiscriminately, specialized teams remove components with remarkable precision. Every valuable system is cataloged, inspected, and preserved for future use. Avionics units, flight-control surfaces, hydraulic systems, wheels, brakes, and landing gear assemblies are removed and prepared for resale or integration into active fleets.

The most valuable assets, however, are often the engines themselves.

In many cases, the Pratt & Whitney PW1000G engines mounted on these aircraft have become more valuable than the operational aircraft. Airlines urgently need replacement engines to keep fleets flying, and the resulting scarcity has dramatically increased demand for serviceable powerplants.

This shift has transformed aircraft teardown operations from a niche activity typically associated with aging aircraft into a major segment of the modern aviation aftermarket.

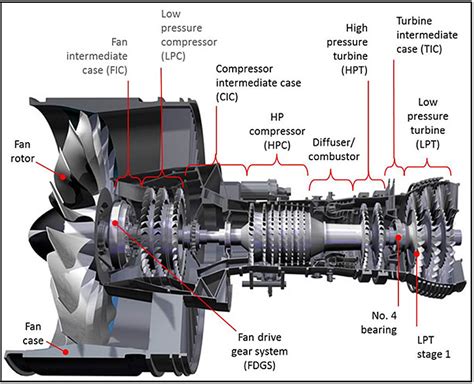

Understanding the Pratt & Whitney GTF Engine Crisis

At the center of the issue lies the Pratt & Whitney PW1000G Geared Turbofan engine family.

When introduced, the GTF represented a revolutionary leap in engine technology. Unlike conventional turbofan engines, the geared turbofan architecture separates fan speed from turbine speed through a reduction gearbox. This allows each component to operate at optimal efficiency, improving fuel burn, reducing emissions, and lowering noise levels.

The technology delivered precisely the performance improvements airlines wanted.

Unfortunately, achieving those gains introduced new technical complexities.

Over time, operators began reporting reliability concerns, maintenance challenges, and unexpected operational disruptions. While these issues initially appeared manageable, the situation escalated dramatically when Pratt & Whitney disclosed a manufacturing defect involving powdered metal used in certain engine components.

The defect created the possibility of microscopic cracks developing within critical engine parts.

As a result, regulators and manufacturers implemented extensive inspection programs affecting hundreds of engines worldwide.

Suddenly, airlines found themselves removing engines from service for inspections that required substantial maintenance resources and lengthy turnaround times.

The impact spread rapidly throughout the global aviation network.

Aircraft that were technically airworthy could not fly because their engines required inspection. Maintenance facilities became overwhelmed. Spare engine inventories disappeared. Repair queues stretched longer than anyone had anticipated.

What began as a manufacturing issue evolved into a worldwide fleet availability crisis.

When Engines Become More Valuable Than Aircraft

Under normal market conditions, a complete aircraft is worth more than the combined value of its individual parts.

The current GTF shortage has temporarily reversed that logic.

Because airlines urgently require replacement engines, serviceable PW1000G engines command exceptionally high lease rates. Industry estimates suggest that a single engine can generate monthly lease revenues approaching $200,000.

For a twin-engine Airbus A321neo, the potential revenue generated by leasing both engines can rival the economics of leasing the entire aircraft.

This unusual equation forces owners to make difficult decisions.

If an aircraft is grounded indefinitely while waiting for maintenance capacity or replacement engines, keeping it intact may generate little or no revenue. Alternatively, removing the engines and placing them into active service elsewhere can immediately create significant financial returns.

The result is a growing number of aircraft being evaluated not as transportation assets but as collections of highly valuable components.

For investors focused on maximizing returns, the math can become compelling.

Rather than waiting years for market conditions to normalize, some owners choose to monetize the aircraft immediately through part-out programs.

This strategy would have seemed almost unimaginable only a few years ago.

How Airlines Are Being Affected

While investors may benefit from rising engine values, airlines face a very different reality.

The shortage of available engines has severely disrupted fleet planning across the industry.

Airlines depend on predictable aircraft availability to schedule routes, allocate crews, and manage capacity. When dozens of aircraft suddenly become unavailable, network planning becomes significantly more complicated.

Many carriers have been forced to retain older aircraft longer than originally planned. Aircraft scheduled for retirement have remained in service because newer replacements cannot operate without engines.

This creates a cascade of operational challenges.

Fuel costs rise because older aircraft are generally less efficient. Maintenance expenses increase as aging fleets require more attention. Fleet commonality suffers. Growth plans must be revised.

Even airlines experiencing strong passenger demand often find themselves unable to fully capitalize on market opportunities because they simply do not have enough operational aircraft available.

The situation is particularly frustrating because demand for air travel remains robust.

Unlike previous aviation downturns where aircraft were parked because passengers disappeared, today’s grounded aircraft are sidelined despite strong market demand.

In many cases, airlines have customers ready to fly but insufficient engine availability to support planned schedules.

The Rise of the Aircraft Teardown Economy

The GTF crisis has inadvertently created a booming new business sector.

Aircraft teardown specialists, component traders, leasing firms, and private-equity investors have all increased their involvement in the aviation aftermarket.

Companies specializing in aircraft dismantling now find themselves operating in an environment where virtually every component has substantial value.

Modern aircraft are remarkably recyclable assets. Engines, avionics, electrical systems, hydraulic components, landing gear assemblies, and flight-control surfaces can often be refurbished and returned to service.

Rather than viewing an aircraft as a single product, teardown firms view it as thousands of individual assets.

Each component possesses its own market value, maintenance history, and demand profile.

The ability to extract, certify, and redistribute those components efficiently has become a major competitive advantage.

Aircraft dismantling is therefore no longer simply about recycling old airframes. It has evolved into a sophisticated supply-chain solution helping airlines obtain critical parts when manufacturers struggle to meet demand.

In many ways, teardown operations have become an essential stabilizing force within the aviation ecosystem.

Why Airbus A321neos Have Become Prime Targets

Not every aircraft type faces the same level of risk.

The Airbus A321neo occupies a particularly important position because it combines extremely strong market demand with heavy exposure to Pratt & Whitney-powered configurations.

The aircraft’s popularity means operators desperately want to keep them flying. At the same time, engine shortages create conditions where serviceable components become exceptionally valuable.

This combination increases the attractiveness of teardown activity.

Owners know that recovered engines can quickly find customers. Airlines need replacement parts immediately. Maintenance providers require inventories to support repair programs.

Consequently, even relatively young aircraft may generate significant returns through component recovery.

The irony is impossible to ignore.

One of the aviation industry’s most technologically advanced and commercially successful aircraft families has become a major source of spare parts precisely because it is so valuable.

Its engines and systems are needed elsewhere across the global fleet.

Spirit Airlines and the Industry’s Growing Debate

The discussion surrounding aircraft dismantling intensified as attention turned toward former Spirit Airlines aircraft.

Spirit operated one of the world’s largest fleets of Airbus A320neo-family aircraft equipped with Pratt & Whitney GTF engines. As the airline’s fleet strategy evolved, industry observers closely monitored what might happen to some of these assets.

Several transactions involving former Spirit aircraft highlighted a broader shift in industry thinking.

Rather than viewing aircraft exclusively as transportation assets, investors increasingly evaluate them through an asset-management lens. Engines, landing gear, avionics, and other components each represent independent sources of value.

This perspective changes how aircraft are bought, sold, and managed.

A modern airliner is no longer merely a machine designed to transport passengers. It is also a portfolio of highly tradable assets whose value can fluctuate according to supply-chain conditions.

In today’s market, engine scarcity has elevated component values to levels few predicted.

As a result, some aircraft owners may ultimately conclude that dismantling an aircraft creates greater financial returns than operating it.

Can the Industry Escape the Crisis?

Most aviation leaders agree that the current situation is unsustainable over the long term.

The idea of dismantling young Airbus A321neos contradicts the fundamental economics that originally justified their purchase. Airlines invested billions of dollars in these aircraft expecting decades of productive service.

Manufacturers likewise designed them to remain operational far into the future.

The solution depends largely on restoring engine availability.

Pratt & Whitney continues expanding maintenance capacity, accelerating inspections, and working to reduce repair backlogs. Industry stakeholders hope these efforts will gradually return more engines to service and reduce the number of grounded aircraft.

Progress is being made, but the scale of the challenge remains substantial.

Hundreds of engines still require inspections, repairs, or maintenance actions. Supply chains remain under pressure. Maintenance facilities continue operating at high utilization levels.

Because of these realities, recovery is expected to occur gradually rather than suddenly.

Until engine availability improves significantly, the economic incentives driving aircraft teardowns are likely to persist.

The Bigger Lesson for Commercial Aviation

The dismantling of young Airbus A321neos reveals a broader truth about modern aviation.

Commercial airlines operate within a highly interconnected ecosystem where manufacturers, engine suppliers, maintenance providers, lessors, investors, and airlines depend on one another.

A disruption affecting a single component can ripple throughout the entire system.

The GTF crisis demonstrates how technological innovation, while delivering extraordinary efficiency gains, can also introduce unexpected vulnerabilities. Aircraft that were designed to save airlines money through lower fuel consumption are now exposing the financial consequences of maintenance bottlenecks and supply-chain constraints.

What makes the situation remarkable is not simply that aircraft are being dismantled.

It is that some of the newest, most efficient airliners in the world are being stripped for parts during a period of strong travel demand and unprecedented aircraft shortages.

Until engine supply stabilizes and maintenance backlogs are resolved, the aviation industry will continue navigating one of the most unusual market distortions in modern commercial aviation history. For now, the value of a Pratt & Whitney GTF engine remains so high that, in certain circumstances, it can outweigh the value of the aircraft built around it.