Flying economy in 2026 is a study in contrasts. Aircraft are more technologically advanced than ever, cabins are quieter, air quality is better, and in-flight entertainment rivals what many people have at home. Yet for millions of passengers, one old problem refuses to disappear: legroom. Seat pitch—the distance between one row of seats and the next—has quietly become one of the most important differentiators between airlines, especially on long-haul routes where hours of immobility can turn discomfort into exhaustion.

Economy class remains the financial backbone of global aviation, but it is also where airlines make their hardest trade-offs. More seats mean more revenue. Fewer inches between rows mean more passengers per flight. Against this economic gravity, only a handful of carriers have chosen to protect legroom as a core part of their brand identity. In 2026, those airlines stand out more sharply than ever.

This is not about marketing slogans or vague promises of comfort. This is about measurable space—inches and centimeters that decide whether knees touch plastic for ten hours straight. From Japan’s meticulous long-haul cabins to select carriers in the Middle East, Asia-Pacific, and North America, a small group of airlines continues to offer economy travelers something increasingly rare: room to breathe.

Why Legroom Has Become the Ultimate Economy Class Luxury

Seat pitch used to be a relatively stable metric. For decades, 33 to 34 inches was common on widebody jets. That baseline eroded steadily as competition intensified and fuel prices rose. By the mid-2010s, 31 inches became the global norm, with some ultra-low-cost carriers pushing as low as 28 inches.

The financial logic is ruthless but simple. Reducing pitch by just one inch can allow an airline to add an extra row of seats. Multiply that by hundreds of aircraft flying thousands of routes, and the revenue impact reaches into the billions. Regulators, including the FAA and EASA, do not mandate minimum seat pitch, leaving comfort decisions entirely in the hands of airlines.

What makes legroom particularly valuable is that passengers notice it immediately, even if they do not consciously measure it. Knees pressed into seatbacks, limited ability to shift posture, and restricted recline all amplify fatigue. On flights exceeding eight hours, legroom often matters more than food quality or entertainment options.

Against this backdrop, the airlines that still offer above-average pitch in economy are not just being generous. They are making a strategic statement about how they want to compete.

Japan Airlines and ANA: The Global Benchmark at 34 Inches

No airlines have defended economy class legroom more consistently than Japan Airlines (JAL) and All Nippon Airways (ANA). Both carriers offer 34 inches (86.4 cm) of pitch across large portions of their long-haul fleets, placing them at the very top of the global rankings in 2026.

JAL’s approach is particularly deliberate. While most airlines embraced nine-abreast seating on the Boeing 787 Dreamliner, JAL resisted the industry trend and retained a 2-4-2 configuration, branded internally as “Sky Wider.” This decision preserves both seat width and legroom, sacrificing density in favor of passenger comfort. The airline pairs this layout with advanced slim-seatback engineering, carving out additional knee space without reducing cushion thickness.

ANA mirrors this philosophy closely, partly due to intense domestic competition and partly due to cultural expectations around service quality. The airline standardized a 34-inch pitch across much of its Boeing 777-300ER and 787 long-haul fleet. In 2026, ANA is rolling out newly designed Recaro economy seats on its Boeing 787-9 aircraft, adding an extra inch of effective knee space and increasing recline to nearly seven inches—one of the most generous figures in global economy class.

These decisions are not accidents. They are rooted in Japan’s concept of omotenashi, a service philosophy centered on anticipating guest needs before they are voiced. For Japanese airlines, legroom is not a cost center. It is a reflection of brand honor.

Emirates: Big Aircraft, Big Space

Emirates occupies a unique position in the global legroom conversation. On its Airbus A380 fleet, economy class passengers enjoy 34 inches of pitch, matching the Japanese carriers at the top of the leaderboard. The sheer scale of the A380 plays a role here. The aircraft’s wide fuselage allows Emirates to maintain comfort while still achieving high overall capacity.

Emirates’ economy experience benefits not just from legroom, but from cabin height, wide aisles, and a sense of openness that narrower aircraft struggle to replicate. While the airline operates tighter configurations on some Boeing 777 variants, its flagship A380 routes remain among the most spacious ways to cross continents in economy class.

The airline’s business model—built around high-volume long-haul connections through Dubai—relies heavily on maintaining a perception of comfort even in its lowest cabin. Legroom is a visible part of that promise.

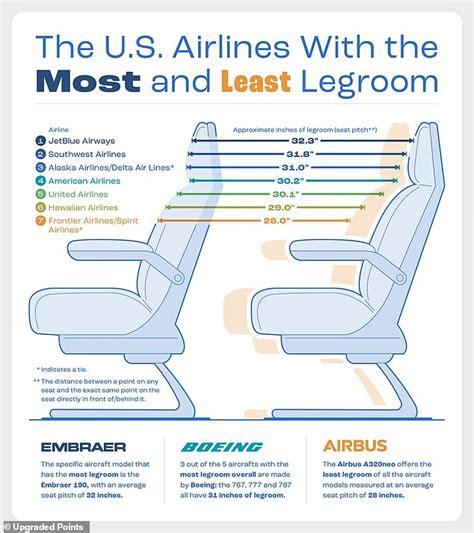

JetBlue: America’s Legroom Outlier

In the United States, JetBlue stands alone. With an average economy pitch of 32.3 inches (82.0 cm), it consistently offers more legroom than any other major US carrier. This is not incidental. It is a core part of JetBlue’s competitive identity.

While legacy airlines focused on seat count and ancillary revenue, JetBlue chose differentiation through comfort. Its Airbus A320 and A321 fleets are configured with fewer rows, allowing for generous pitch even on standard economy tickets. Combined with free high-speed Wi-Fi and seatback entertainment across the fleet, JetBlue delivers what many travelers consider the most humane economy experience in North America.

In a market defined by razor-thin margins and relentless cost pressure, JetBlue’s decision to protect legroom is a strategic gamble that continues to pay dividends in customer loyalty.

The Upper Middle Tier: Asia-Pacific Excellence at 32 Inches

A cluster of respected international airlines occupies the next tier, offering 32 inches of pitch—noticeably better than the global average, though slightly behind the leaders. Singapore Airlines, Cathay Pacific, and Qantas all fall into this category.

These carriers balance comfort with density by adopting nine-abreast seating on most widebody aircraft, including the Airbus A350 and Boeing 787. The result is a cabin that feels refined and well-designed, even if it lacks the outright spaciousness of Japanese or A380-equipped Emirates cabins.

What elevates these airlines is not just legroom, but the overall economy experience. High-quality meals, attentive service, and thoughtfully designed seats compensate for the missing inches. On long-haul routes, this combination often feels more comfortable than tighter cabins with inferior service.

Southwest, Delta, and Alaska: The US Standard Bearers

Among US carriers, Southwest Airlines offers 31.8 inches, while Delta Air Lines and Alaska Airlines sit at 31 inches. These figures reflect the practical ceiling of comfort in a market dominated by price competition.

Delta earns strong passenger satisfaction despite average legroom thanks to operational reliability and a consistently polished onboard product. Alaska pairs similar pitch with a well-regarded soft product and strong regional loyalty. Southwest’s open seating model and historically generous policies have helped offset tighter dimensions, though changes to its free services in 2026 have begun to shift perceptions.

None of these airlines lead on legroom, but all remain meaningfully better than the ultra-low-cost segment.

Why Slim Seats Haven’t Solved the Problem

Seat manufacturers often argue that modern slim-back designs make traditional pitch measurements less relevant. Thinner seat shells and sculpted backs can increase perceived knee room even at tighter spacing. There is some truth to this. A well-designed 31-inch seat can feel comparable to an older 33-inch model.

However, perception has limits. On long-haul flights, actual pitch still governs posture, circulation, and the ability to shift positions. Recline angles, tray table usability, and knee clearance during sleep all depend on real space, not marketing diagrams. Slim seats soften the blow, but they do not erase it.

The Cautionary Tale of ‘More Room Throughout Coach’

In 2000, American Airlines attempted something radical. Its “More Room Throughout Coach” initiative removed thousands of seats from its fleet, increasing pitch to 34–35 inches across the entire economy cabin. Passenger feedback was overwhelmingly positive. Financial results were not.

Despite widespread praise, American discovered that customers were unwilling to pay even modestly higher fares for extra legroom. Compounded by the post-9/11 downturn, rising fuel costs, and fierce low-cost competition, the initiative was scrapped by 2004. The program’s failure became a cautionary legend within the industry, cited repeatedly by executives as proof that comfort does not sell—at least not at scale.

That lesson continues to shape economy cabins in 2026.

Why Japan Still Defies the Economics

Japanese airlines are the rare exception because their business model is different. Higher yields, strong brand loyalty, and cultural expectations around service quality allow carriers like JAL and ANA to prioritize comfort without eroding profitability. Their focus is not on squeezing maximum passengers onto each aircraft, but on maximizing return per seat through reputation and repeat business.

In a global industry obsessed with density, Japan remains a quiet counterexample.

The 2026 Economy Legroom Leaderboard

At the top sit Japan Airlines, All Nippon Airways, and Emirates, each offering 34 inches on key aircraft. JetBlue leads the United States at 32.3 inches, followed closely by Singapore Airlines, Cathay Pacific, and Qantas at 32 inches. Southwest, Delta, and Alaska round out the top ten just above the industry average.

These airlines are not just selling tickets. They are selling tolerance for time. On flights that stretch past ten hours, those extra inches translate into real physical relief—and that, in 2026, has become one of the most valuable commodities in economy class.

Legroom is no longer a trivial spec buried in seat maps. It is a quiet statement of intent. The airlines that still offer it are telling passengers exactly where they stand.