The Strait of Hormuz, a critical chokepoint for global oil transport, is at the heart of a looming energy crisis. With escalating tensions following U.S. military strikes on Iran’s nuclear sites, Tehran has signaled a potential closure of this strategic maritime artery. If executed, the fallout would be seismic, especially for Asia’s largest energy consumers — China, India, and South Korea — who collectively depend on this passage for the lion’s share of their oil imports.

Each day, nearly 20 percent of global oil production — equivalent to 14.2 million barrels of crude oil and 5.9 million barrels of refined petroleum products — sails through the Strait of Hormuz. A staggering 84 percent of that output is bound for Asian markets, according to the U.S. Energy Information Administration (EIA). With virtually all Middle Eastern oil — from Saudi Arabia, Iraq, Kuwait, Qatar, the UAE, and even Iran itself — flowing through this single channel, any disruption threatens not just regional stability, but the very foundation of Asia’s industrial and economic machinery.

China’s Oil Arteries Flow Through Hormuz

As the world’s largest oil importer, China stands to lose the most. In the first quarter of 2025, Beijing received 5.4 million barrels per day (bpd) of crude via the Strait of Hormuz, underscoring just how embedded Middle Eastern oil is in its energy matrix.

Saudi Arabia, China’s second-largest oil partner, supplies approximately 1.6 million bpd, accounting for around 15 percent of China’s total crude imports. Meanwhile, despite sanctions and diplomatic complexities, China remains the dominant buyer of Iranian oil, absorbing over 90 percent of Tehran’s exports. In April 2025 alone, China imported 1.3 million bpd of Iranian crude, showcasing the intricate entanglement between China’s energy security and Persian Gulf geopolitics.

The closure of Hormuz would compel Beijing to ramp up sourcing from alternative suppliers — including Russia and Venezuela — while contending with logistical constraints, higher freight costs, and potential price surges.

India’s Dependence Runs Deep

Second in line to face serious repercussions is India, whose reliance on Gulf oil is both strategic and economic. According to the EIA, 2.1 million bpd of India’s crude imports passed through the Strait during the first quarter of 2025. In total, 53 percent of India’s oil came from Middle Eastern nations — chiefly Iraq and Saudi Arabia.

India has tried to diversify its energy portfolio over recent years, most notably increasing imports of discounted Russian crude amidst Western sanctions. However, this shift only partially insulates New Delhi. Minister of Petroleum and Natural Gas, Hardeep Singh Puri, acknowledged the volatility of the current environment, emphasizing that while India has diversified, a significant portion of its oil still transits through Hormuz.

“We will take all necessary steps to ensure the stability of supplies of fuel to our citizens,” Puri noted, underscoring the government’s strategic reserves and diplomatic engagements.

South Korea Braces for Impact

South Korea, Asia’s fourth-largest economy, imports roughly 1.7 million bpd through Hormuz, amounting to 68 percent of its total crude oil intake. Its dependency is especially acute when viewed through the lens of supplier concentration — Saudi Arabia alone delivers over 33 percent of Seoul’s crude.

While the South Korean Ministry of Trade, Industry and Energy maintains that there have been no immediate disruptions, it has warned of looming vulnerabilities. To counteract these, South Korea has activated contingency plans including a strategic petroleum reserve equivalent to 200 days of supply, one of the most substantial in the region.

Energy firms are also realigning logistics and exploring non-Middle Eastern sources — a complicated maneuver given the infrastructural and commercial limitations.

Japan’s Cautious Navigation Through Crisis

Japan, while somewhat less dependent than its Asian neighbors, remains deeply entwined in the Gulf supply chain. The EIA reports 1.6 million bpd of Japanese oil imports came via Hormuz in early 2025. Customs data shows that a staggering 95 percent of Japan’s crude last year originated from the Middle East.

Japanese energy firms, notably Mitsui OSK Lines, are responding with preemptive adjustments. Tankers are being rerouted and repositioned to minimize their exposure in Gulf waters. The Japanese government is also working closely with private stakeholders to implement crisis mitigation strategies, though full-scale contingency plans remain tightly guarded.

Other Asian Importers in the Firing Line

Beyond the major players, several other Asian economies — notably Thailand and the Philippines — receive a combined 2 million bpd via Hormuz. While their absolute volumes are lower, these countries are typically more vulnerable to price shocks and supply disruptions due to smaller strategic reserves and higher dependency ratios.

Europe and the United States also receive minor volumes through Hormuz — approximately 0.5 million and 0.4 million bpd, respectively — but they are better positioned to handle short-term disruptions via diverse supply chains and larger domestic production.

Limited Alternatives, Global Consequences

Can the world adjust if Iran closes the Strait of Hormuz? Technically, yes — but not without significant costs and chaos. While some Gulf producers like Saudi Arabia and the UAE have limited infrastructure to bypass Hormuz — such as the East-West Pipeline and Abu Dhabi Crude Oil Pipeline — their combined capacity is only about 2.6 million bpd, far short of the region’s total output.

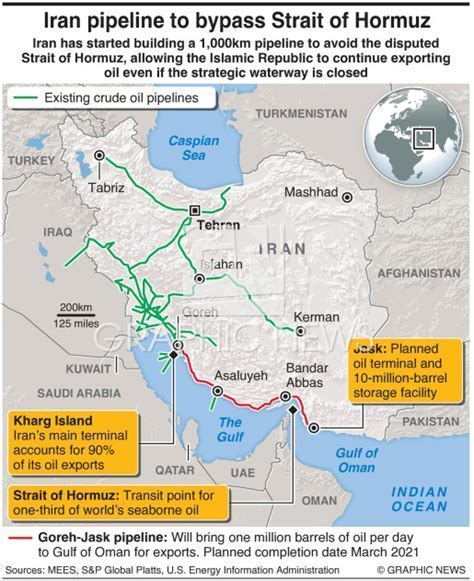

Iran’s Ghorbani-Jask pipeline, intended to export oil via the Gulf of Oman, offers minimal relief with a maximum output of just 300,000 bpd, and it has been inactive since last year.

Experts at MUFG Bank point to global oil inventories, OPEC+ spare capacity, and U.S. shale oil as potential buffers. However, these are short-term mitigants. Most of the spare production capacity remains geographically stuck within the very Persian Gulf area that would be sealed off.

The Bottom Line: Asia’s Oil Lifeline is Iran’s Leverage

The strategic calculus behind a Strait of Hormuz closure is clear: Iran’s most powerful weapon isn’t just military — it’s geographical. The mere threat of closure sends oil prices climbing and energy security strategies into overdrive. For China, India, and South Korea, whose economic growth is closely tied to uninterrupted energy flow, the stakes are monumental.

Even short-term disruptions could induce supply crunches, inflationary pressure, and political backlash at home. While strategic reserves and supplier diversification can provide temporary cover, the asymmetry of risk is undeniable. Iran’s grip on Hormuz remains a sharp reminder that energy dependence and geopolitics are deeply and perilously intertwined.

As diplomacy intensifies behind closed doors and military deployments rise in the Gulf, the question isn’t just whether Iran will close the Strait — but whether the world is ready if it does.