The image of aircraft retirement used to be predictable: aging jets, worn interiors, and decades of service culminating in a quiet exit to desert storage or scrapyards. That narrative no longer holds. Across global fleets, relatively young aircraft—some barely past their first heavy maintenance cycle—are being withdrawn from service. Models like the Airbus A320neo and Airbus A220, designed for efficiency and longevity, are now at the center of a paradox where modernity does not guarantee longevity.

This shift is not driven by structural fatigue or obsolescence in the traditional sense. Instead, it reflects a deeper transformation in aviation economics, where engines, supply chains, leasing structures, and operational reliability outweigh the age of the airframe itself. The aircraft, once treated as a unified asset, is increasingly evaluated as a collection of high-value components—each with its own market dynamics.

At the core of this transformation lies a simple but powerful reality: an aircraft that cannot reliably fly is no longer an asset—it becomes a liability. When operational uncertainty collides with rising component values, the logic of early retirement begins to make uncomfortable but compelling sense.

Engine Reliability Challenges Driving Early Aircraft Retirement

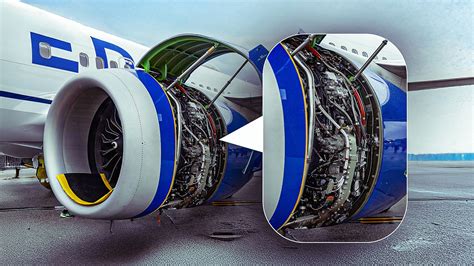

The promise of next-generation engines was clear: lower fuel burn, reduced emissions, and quieter operations. Yet, in practice, these technological advancements have introduced a new layer of complexity that has proven difficult to manage at scale. Engines such as the Pratt & Whitney PW1000G geared turbofan have encountered persistent issues, including premature component wear and contamination in critical parts.

These are not minor inconveniences. They translate directly into grounded aircraft, extended maintenance cycles, and unpredictable availability. Airlines operating fleets dependent on these engines have faced repeated disruptions. In some cases, entire sub-fleets have been sidelined, not because the aircraft themselves are compromised, but because the engines cannot be relied upon to perform consistently.

For operators, this creates a cascading problem. Flight schedules must be adjusted, spare capacity becomes scarce, and customer confidence can erode quickly. Even a technically “young” aircraft becomes operationally old if it cannot deliver consistent uptime. This is why airlines such as Air Austral have made the difficult decision to phase out relatively new aircraft like the A220—not due to age, but due to the disproportionate operational burden imposed by engine reliability issues.

The Surging Value of Aircraft Engines in a Supply-Constrained Market

A quiet revolution is underway in how aircraft are valued, and it begins with the engine. Traditionally, the airframe represented the bulk of an aircraft’s worth, with engines considered essential but secondary components. That hierarchy has flipped. In today’s constrained market, engines are often the most valuable part of the aircraft—by a significant margin.

The reasons are rooted in scarcity. Supply chain disruptions, limited maintenance capacity, and ongoing technical issues have created a global shortage of serviceable engines. As a result, the market value of engines—particularly those powering popular narrowbody jets—has surged dramatically. A single operational engine can command $10–15 million, placing a pair of engines on par with, or even exceeding, the residual value of the entire aircraft.

This imbalance creates a powerful financial incentive. Instead of deploying an aircraft for passenger service, owners may achieve higher returns by removing the engines and leasing or selling them independently. Airlines in urgent need of spare engines are willing to pay premiums to keep their fleets operational, further reinforcing this trend.

The result is a market dynamic where the aircraft itself becomes secondary. When engines alone can generate faster and more reliable returns, the rationale for keeping the full aircraft in service begins to erode.

Aircraft Part-Out Strategies: When Dismantling Becomes Profitable

The concept of “parting out” an aircraft is not new, but its application to relatively young jets is a striking development. Specialized firms now dismantle aircraft and recover high-value components, from engines and landing gear to avionics and auxiliary power units. These parts are then certified and reintroduced into the global supply chain.

What has changed is the age at which this process occurs. Historically, part-out operations were reserved for aircraft nearing the end of their economic life—typically after two decades or more in service. Today, aircraft as young as five to eight years are being dismantled, driven largely by the outsized value of their engines.

This shift reflects a recalibration of priorities. Instead of maximizing long-term operational revenue, asset owners are increasingly focused on short-term value extraction. If the sum of an aircraft’s parts exceeds its projected earnings in service, dismantling becomes the logical choice.

There is also a strategic dimension. By releasing high-demand components into the market, lessors and asset managers can respond to immediate shortages while positioning themselves for future opportunities. In this context, the aircraft is no longer a long-term commitment—it is a flexible financial instrument.

Leasing Dynamics and the Pressure to Maximize Asset Returns

A significant portion of the global fleet is not owned by airlines but by leasing companies. These entities operate under a different set of incentives, prioritizing return on investment, asset liquidity, and market timing. When evaluating an aircraft’s future, they are less concerned with operational sentiment and more focused on financial performance.

If an aircraft becomes difficult to place with airlines—due to reliability concerns or shifting market preferences—its leasing potential declines. At the same time, the rising value of individual components, particularly engines, offers an alternative path to profitability. In such scenarios, dismantling the aircraft can deliver faster, more predictable returns than attempting to secure a new lease.

This creates a subtle but powerful pressure on the system. Airlines may prefer to retain aircraft for operational continuity, but lessors ultimately control the asset. When the financial case for part-out becomes compelling, early retirement is often the outcome.

The implications extend beyond individual aircraft. Leasing strategies influence fleet composition, availability of spare parts, and even the pace at which new aircraft are introduced. In a market shaped by these dynamics, age becomes a secondary consideration—what matters is economic performance in the present moment.

Operational Disruptions and the True Cost of Grounded Aircraft

Aircraft generate revenue only when they are airborne. Every hour spent on the ground represents lost income, compounded by ongoing costs such as leasing fees, maintenance obligations, and parking charges. When technical issues—particularly engine-related—force aircraft out of service for extended periods, the financial impact escalates بسرعة.

For airlines, the challenge is not just the direct cost of downtime, but the ripple effects across the network. Schedules must be reconfigured, replacement aircraft sourced, and passenger disruptions managed. In some cases, airlines are forced to lease short-term replacements at premium rates, further eroding profitability.

Reliability, therefore, becomes a decisive factor. An aircraft that cannot be counted on to operate consistently introduces uncertainty into every aspect of the business. Over time, this uncertainty can outweigh the benefits of keeping the aircraft in service, even if it is relatively new.

This is why early retirement can emerge as a pragmatic solution. By removing problematic aircraft from the fleet, airlines can stabilize operations, reduce exposure to unexpected disruptions, and focus on assets that deliver consistent performance. It is not a decision taken lightly—but in many cases, it is the most rational path forward.

Supply Chain Constraints Amplifying Early Retirement Trends

The broader aviation ecosystem has been under strain since the early 2020s, with supply chain disruptions affecting manufacturers, maintenance providers, and operators alike. Delays in aircraft deliveries, shortages of critical components, and limited repair capacity have created bottlenecks that ripple across the industry.

Engine maintenance has been particularly affected. Turnaround times for inspections and repairs have stretched from weeks to months, and in some cases, even longer. Maintenance backlogs continue to grow, leaving airlines with aircraft that cannot return to service in a timely manner.

These constraints exacerbate existing challenges. When engines cannot be repaired quickly and replacements are unavailable, the economic viability of keeping certain aircraft diminishes rapidly. Airlines and lessors are left with difficult choices: wait indefinitely for repairs, or extract value through dismantling.

At the same time, delays in new aircraft deliveries limit the ability to replace grounded jets. Popular models like the A320neo remain in high demand, but production constraints mean that replacements are not always readily available. This creates a paradox where airlines need capacity but cannot rely on existing or incoming aircraft to provide it.

In this environment, early retirement is not simply a response to isolated issues—it is part of a broader adaptation to systemic constraints. The industry is recalibrating, finding new ways to balance operational needs with financial realities.

A Fundamental Shift in How Aircraft Are Valued

The early retirement of modern aircraft signals a deeper transformation in aviation. The traditional lifecycle—purchase, operate for decades, then retire—has been disrupted by a more dynamic and fragmented model. Aircraft are now evaluated not just as operational tools, but as portfolios of assets with fluctuating market values.

Engines, once integrated components, have become standalone commodities. Maintenance capacity has become a strategic bottleneck. Leasing decisions are increasingly driven by short-term market conditions rather than long-term planning. Together, these factors are reshaping how airlines and lessors think about fleet management.

What emerges is a more fluid system, where flexibility and responsiveness take precedence over longevity. Aircraft may enter service with the expectation of a long career, but their fate is ultimately determined by forces that extend far beyond the airframe itself.

For passengers, this shift is largely invisible. Flights continue, schedules adjust, and new aircraft enter service. But behind the scenes, the calculus has changed. The decision to retire an aircraft is no longer about age—it is about value, reliability, and timing in a rapidly evolving market.

And in that market, even the newest aircraft are not immune to an early exit.